Summary

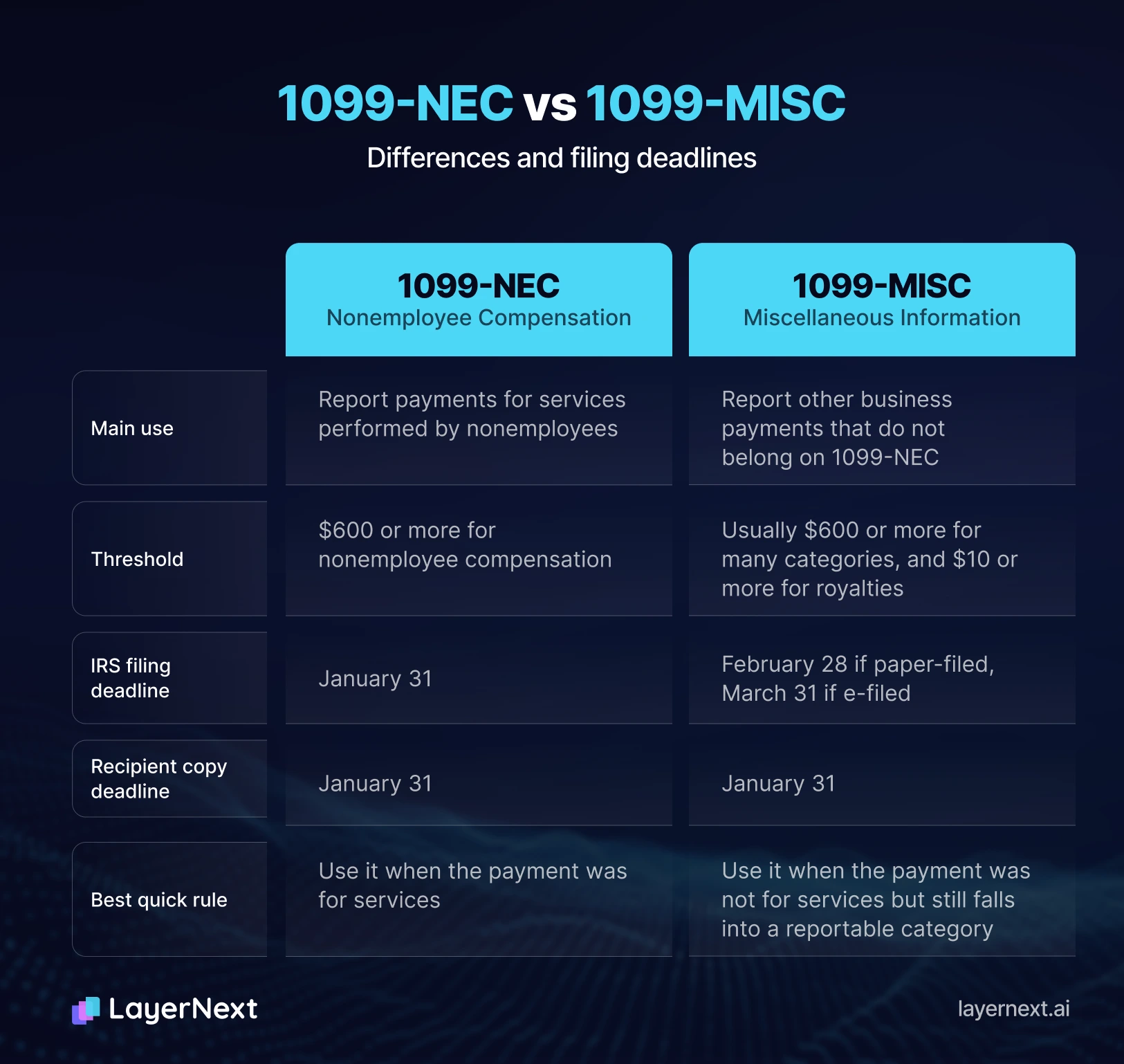

Form 1099-NEC and Form 1099-MISC are both used to report business payments, but they are not interchangeable. In general, 1099-NEC is for nonemployee compensation, meaning payments for services performed by someone who is not your employee. 1099-MISC is for other reportable payments, such as rent, royalties, prizes, medical payments, and certain attorney-related payments. The easiest way to choose the right form is to ask whether the payment was for services. If yes, start with 1099-NEC. If not, check whether the payment fits one of the 1099-MISC categories. Under current IRS instructions, most common reporting thresholds remain $600, while royalties on Form 1099-MISC are generally reportable at $10 or more.

- Use 1099-NEC for contractor, freelancer, consultant, and many attorney service payments of $600 or more.

- Use 1099-MISC for rents, royalties, other income, medical and health care payments, crop insurance proceeds, and gross proceeds paid to an attorney.

- Do not use either form for employees. Employee pay belongs on Form W-2.

- Credit card and third-party network payments are generally reported on Form 1099-K instead, not on 1099-NEC or 1099-MISC.

- If you file 10 or more information returns in aggregate, the IRS requires electronic filing.

What is Form 1099-NEC?

Form 1099-NEC is the IRS form used to report nonemployee compensation. That usually means payments made in the course of a trade or business to someone who is not an employee, such as a freelancer, consultant, designer, virtual assistant, or independent contractor. The IRS says Form 1099-NEC generally applies when you paid at least $600 for services, including certain payments to attorneys.

The key point is simple

If the payment was for services performed by a nonemployee, 1099-NEC is usually the right form.

What is Form 1099-MISC?

Form 1099-MISC is the IRS form used to report miscellaneous information payments. That means payments made in the course of a trade or business that don’t fall under nonemployee compensation, such as rent, prizes and awards, medical and health care payments, crop insurance proceeds, or payments to an attorney in a settlement. The IRS says Form 1099-MISC generally applies when you paid at least $600 in most of these categories, though royalties have a lower threshold of $10.

The key point is simple

If the payment was for something other than services performed by a nonemployee, think rent, royalties, or other miscellaneous income , 1099-MISC is usually the right form.

1099-MISC vs 1099-NEC: the core difference

Form 1099-MISC is still widely used, but for a different set of payments. The IRS says it is used to report royalties, rents, prizes and awards, other income payments, medical and health care payments, crop insurance proceeds, fishing boat proceeds, and gross proceeds paid to an attorney. Most of these categories are reportable at $600 or more, while royalties are generally reportable at $10 or more.

So the practical rule is this

1099-NEC is mainly for services, while 1099-MISC is mainly for other reportable business payments that do not belong on 1099-NEC.

When to use each form

Use 1099-NEC when all or most of the following are true: the recipient is not your employee, the payment was for services, the payment was made in the course of your business, and the total paid met the reporting threshold. Use 1099-MISC when the payment was not for nonemployee services but falls into one of the IRS miscellaneous categories, such as rent or medical payments.

One of the most common filing mistakes involves attorneys. The IRS says attorneys’ fees for legal services are generally reported on 1099-NEC, while gross proceeds paid to an attorney, such as certain settlement-related payments, are generally reported on 1099-MISC box 10.

Another common mistake is reporting card or marketplace payments on the wrong form. Payments made by credit card, payment card, or certain third-party networks are generally reported by the payment settlement entity on Form 1099-K, not by the payer on 1099-NEC or 1099-MISC.

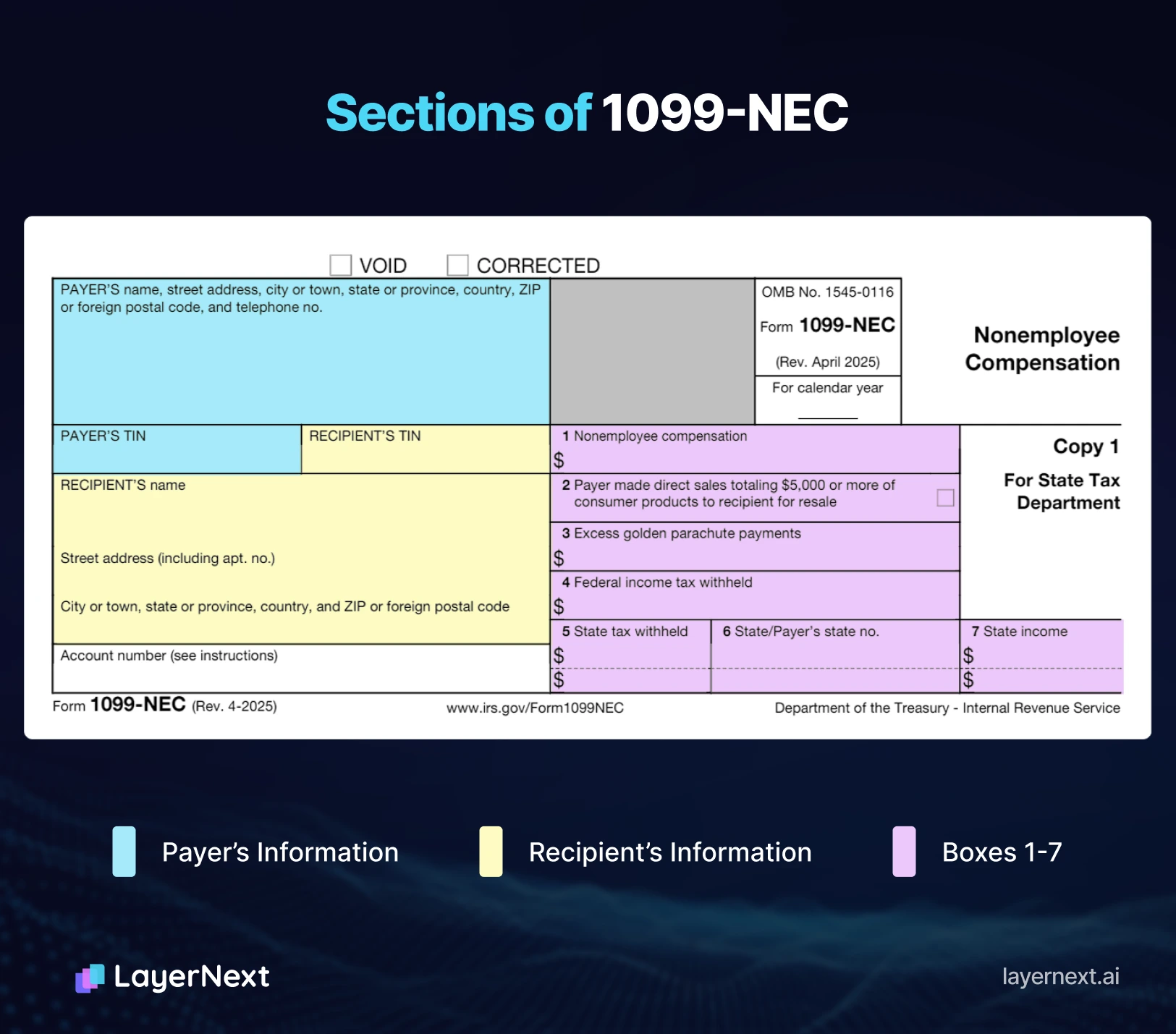

How to fill out Form 1099-NEC

Start by gathering the payer’s legal name, address, telephone number, and TIN, along with the recipient’s name, address, and TIN. The current IRS form also includes an optional account number field and a 2nd TIN notice checkbox.

Then complete the key boxes:

- Box 1: Enter nonemployee compensation of $600 or more. This includes fees, commissions, prizes for services, and other compensation for services performed for your business by a nonemployee.

- Box 2: Check this box only if you made direct sales totaling $5,000 or more of consumer products for resale. Do not enter a dollar amount here.

- Box 3: Enter excess golden parachute payments, if applicable.

- Box 4: Enter backup withholding, if any federal income tax was withheld.

- Boxes 5 through 7: Use these state reporting boxes if needed. The IRS says they are provided for convenience and do not need to be completed for the IRS itself.

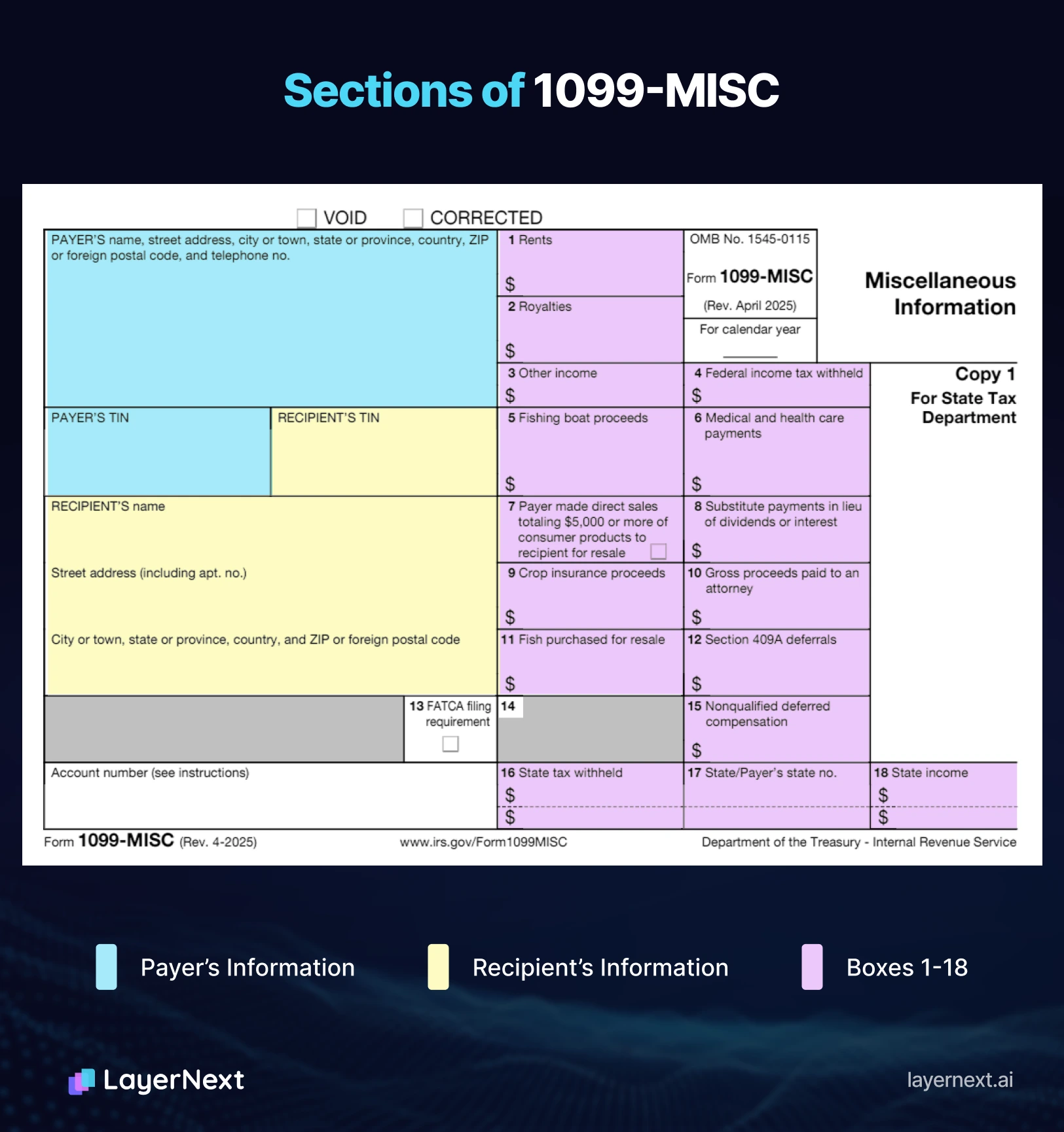

How to fill out Form 1099-MISC

Just like 1099-NEC, begin with payer and recipient names, addresses, and TINs. The form also includes an account number field and a 2nd TIN notice checkbox.

Then enter the payment in the correct box:

- Box 1 for rents

- Box 2 for royalties

- Box 3 for other income

- Box 4 for federal income tax withheld

- Box 6 for medical and health care payments

- Box 8 for substitute payments in lieu of dividends or interest

- Box 9 for crop insurance proceeds

- Box 10 for gross proceeds paid to an attorney

- Boxes 16 through 18 for state information, when relevant

The most important rule when filling out Form 1099-MISC is to put the payment in the correct box. The IRS explicitly warns filers to report each payment in the proper box because the agency uses that information to determine whether the recipient reported it correctly.

Forms 1099-MISC vs. 1099-NEC: when and how to file each

The IRS says Form 1099-NEC is due January 31, whether you file on paper or electronically. Form 1099-MISC is due February 28 if filed on paper, or March 31 if filed electronically. Recipient statements are generally due by January 31 for both forms.

If you file on paper, the IRS says Form 1099-NEC must be submitted with Form 1096, and if you file more than one type of information return on paper, you need a separate Form 1096 for each type.

There is one more important filing detail. The IRS states that the red Copy A downloadable from its site is for informational purposes and should not be printed and filed with the IRS. You can print recipient copies from the IRS website, but for IRS filing you need official scannable forms or electronic filing.

Best practices for Forms 1099-MISC or 1099-NEC

The best time to get 1099 compliance right is before year-end. Collect a signed Form W-9 before the first payment so you have the payee’s legal name and TIN on file. The IRS instructions specifically reference using Form W-9 to obtain a TIN, including for attorneys.

Next, track payment method carefully. If a vendor was paid through a credit card or third-party platform, that payment may fall under Form 1099-K instead, so recording the payment channel helps prevent duplicate reporting.

It also helps to review vendor totals quarterly, separate attorney fees from attorney gross proceeds, and file electronically when possible. The IRS requires e-filing once you hit 10 or more information returns in the aggregate, and electronic filing reduces deadline pressure and mailing issues.

Penalties for incorrect or late filings on 1099 forms

The IRS imposes separate penalties for failing to file a correct information return on time and for failing to provide a correct payee statement on time. For returns due in 2026, the IRS penalty table lists $60 per return if filed up to 30 days late, $130 per return if filed between 31 days late and August 1, $340 per return if filed after August 1 or not filed, and $680 per return for intentional disregard. These amounts can change by year, so it is worth checking the current penalty table before filing season.

That makes accuracy just as important as speed. Filing the wrong form, putting payments in the wrong box, using the wrong TIN, or missing the recipient statement deadline can all create avoidable cleanup work and extra cost.

How We Help Businesses Stay 1099-Ready

At LayerNext, we help reduce the mess that usually builds up long before 1099 season starts. Missing W-9s, uncategorized vendor payments, scattered receipts, and incomplete records can all make year-end reporting harder than it needs to be.

We keep bookkeeping current through real-time reconciliation, document capture, transaction categorization, and tax-ready reporting. By keeping books updated throughout the year, we make it easier to review vendor payments, organize supporting documents, and prepare for 1099 reporting with fewer manual cleanups.

Our focus is on helping small businesses stay organized, maintain clearer financial records, and approach tax season with more confidence.

FAQ