Summary

Nonprofit bookkeeping is not just a compliance obligation. It is the foundation of organizational credibility, donor trust, and grant eligibility. Unlike for-profit accounting, it demands strict separation of restricted and unrestricted funds, functional expense allocation, and four distinct financial statements.

- Fund tracking is non-negotiable: restricted donor funds must be coded on receipt and spent only as designated. Misuse can trigger repayment demands, lost grants, and legal exposure.

- Four financial statements are required: the Statement of Financial Position, Statement of Activities, Statement of Functional Expenses, and Statement of Cash Flows are all essential for audits and board governance.

- Form 990 is your public financial record: the version you file depends on gross receipts, and missing three consecutive filings triggers automatic loss of tax-exempt status.

- Payroll allocation is where most errors happen: staff time must be split across program, admin, and fundraising functions. Coding everything to 'program' to improve overhead ratios is a red flag auditors will catch.

- Monthly reconciliation beats annual scrambles: reviewing restricted fund balances, reconciling accounts, and filing payroll taxes monthly prevents the costly errors that surface at grant reporting time.

Running a nonprofit means every dollar has a story. A grant from a foundation, a donation from an individual, a program fee from a workshop, each one comes with expectations about how it gets spent, tracked, and reported. Miss a filing deadline, misclassify a restricted fund, or hand your board an inaccurate financial statement, and the consequences range from losing donor trust to losing your tax-exempt status entirely.

Nonprofit bookkeeping isn't just a compliance obligation. It's the foundation that makes everything else possible, grant applications, audits, board governance, donor reporting, and long-term financial health. And yet most small to mid-size nonprofits treat it as an afterthought, outsourced to a volunteer treasurer or handled in a spreadsheet that hasn't been reconciled in months.

This guide covers exactly how nonprofit bookkeeping differs from for-profit accounting, what accounts and reports you actually need, and how to stay compliant with IRS requirements year-round, without hiring a full-time accountant.

How Nonprofit Accounting Differs From For-Profit Accounting

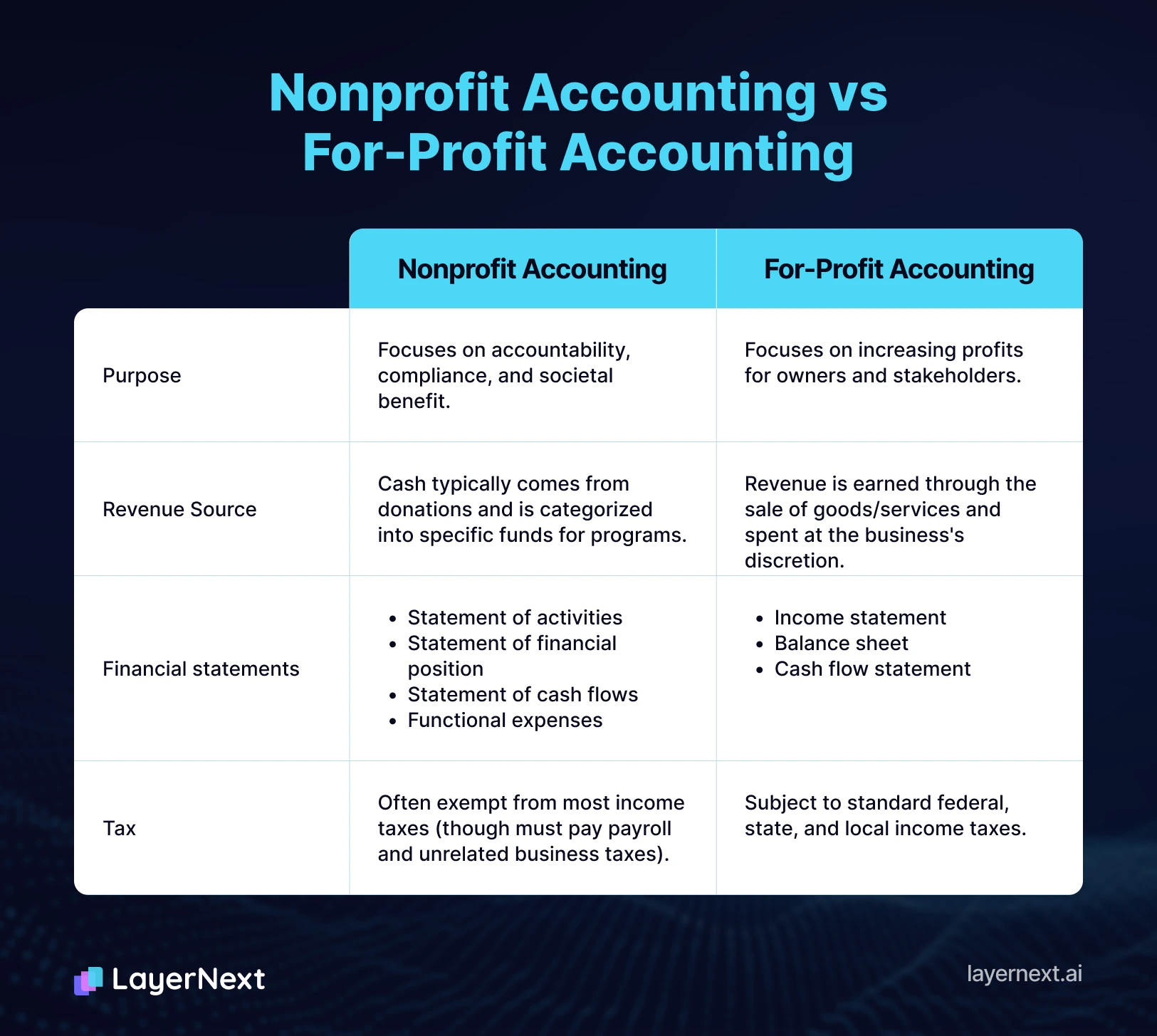

The fundamental difference comes down to purpose. A for-profit business exists to generate profit for its owners. A nonprofit exists to advance a mission, and its financial reporting has to reflect that.

This creates four structural differences that shape everything about how nonprofit books are set up:

No equity accounts — only net assets

For-profit businesses have owner's equity or shareholder equity on their balance sheet. Nonprofits don't have owners. Instead, the equivalent is called net assets, and the Financial Accounting Standards Board (FASB) requires nonprofits to classify net assets into two categories under ASC 958: net assets without donor restrictions and net assets with donor restrictions.

Restricted vs unrestricted funds

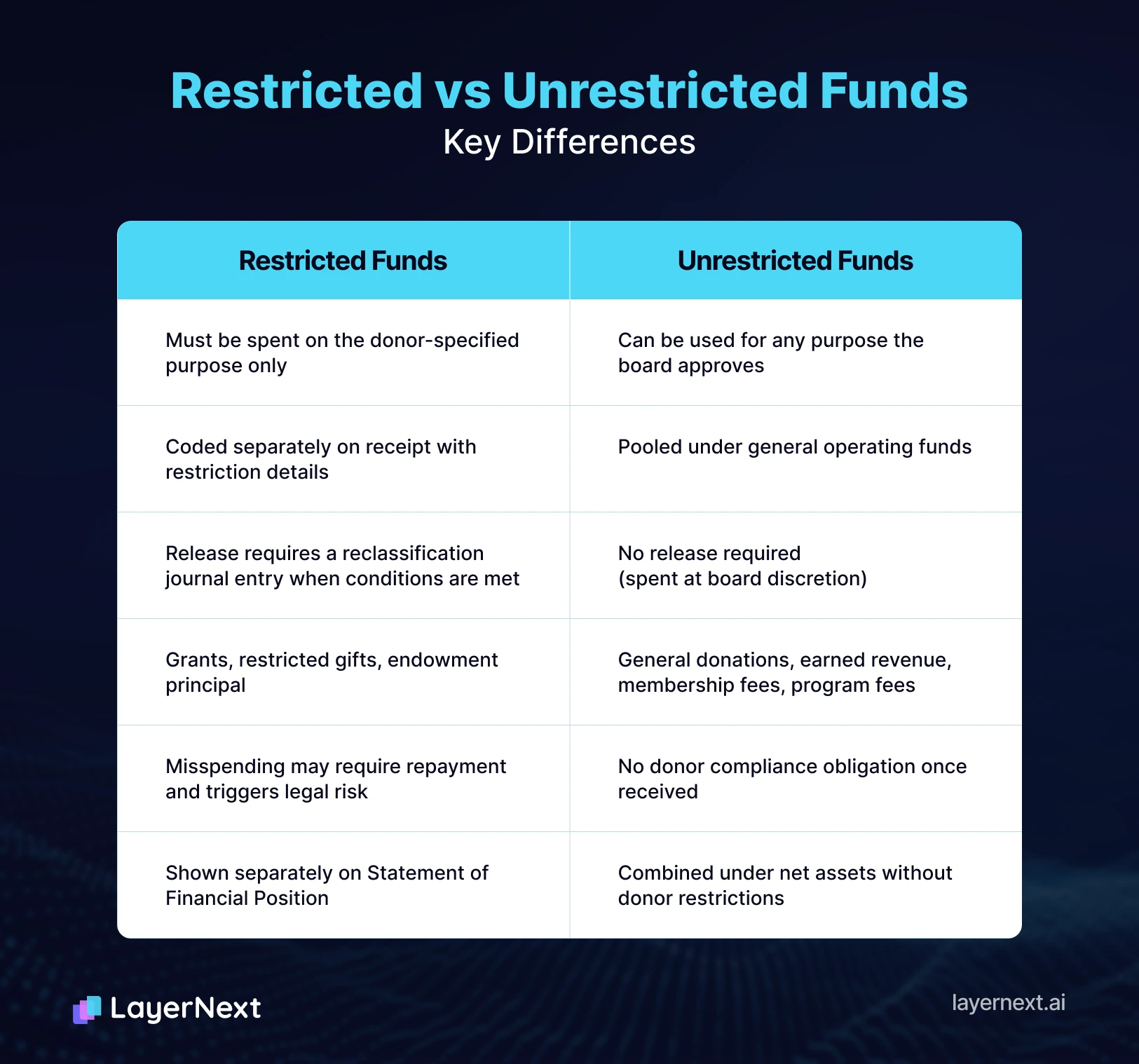

This is the defining complexity of nonprofit bookkeeping. A donor who gives $10,000 "for the children's literacy program" has placed a restriction on those funds, they cannot be used for general operating expenses, even if the organization desperately needs the money elsewhere. Tracking restricted and unrestricted funds separately, and ensuring restricted funds are spent only on their designated purpose, is a legal obligation, not just good practice.

Fund accounting

Many nonprofits use fund accounting, which tracks resources in separate "funds" based on their source and purpose rather than pooling everything into one account. Each fund is essentially a self-contained mini balance sheet. While not all small nonprofits need full fund accounting, understanding the concept is essential to understanding why nonprofit bookkeeping is structured differently.

Different financial statements

For-profit businesses produce a balance sheet, income statement, and cash flow statement. Nonprofits produce a Statement of Financial Position (the nonprofit equivalent of a balance sheet), a Statement of Activities (the nonprofit equivalent of an income statement), a Statement of Cash Flows, and, for organizations with multiple programs, a Statement of Functional Expenses. All four are required if your nonprofit undergoes an audit.

The Chart of Accounts Every Nonprofit Needs

Your chart of accounts for a nonprofit needs to reflect the distinction between restricted and unrestricted activity, program vs administrative costs, and the various sources of income a nonprofit typically has.

Revenue and support accounts

- Individual contributions : unrestricted

- Individual contributions : temporarily restricted

- Foundation grants : unrestricted

- Foundation grants : restricted (by grant name or project)

- Government grants and contracts

- Program service revenue (fees charged for services)

- Special event revenue (gross, before event expenses)

- In-kind contributions (donated goods and services at fair value)

- Investment income and interest

Expense accounts — by function

The IRS and FASB both require nonprofits to classify expenses by function: program services (the actual mission work), management and general (overhead), and fundraising. This functional allocation feeds directly into Form 990 and is one of the primary things donors and watchdog organizations examine.

- Program expenses (one sub-account per program)

- Management and general expenses (executive salaries, accounting, legal, office)

- Fundraising expenses (donor communications, event costs, grant writing)

Net asset accounts

- Net assets without donor restrictions

- Net assets with donor restrictions (one sub-account per restriction)

Liability accounts

- Accounts payable

- Deferred revenue (grants received but not yet earned)

- Refundable advances

The key discipline: every transaction needs to be coded not just to an account, but to a function (program, management, or fundraising) and to a fund or restriction class. This is what makes nonprofit bookkeeping more complex than small business bookkeeping, and what most general-purpose accounting software isn't set up to handle cleanly out of the box.

Restricted vs Unrestricted Funds: The Rule You Cannot Get Wrong

This is the most consequential distinction in nonprofit finance, and mishandling it is one of the most common reasons nonprofits run into legal and donor relations problems.

Temporarily restricted funds

Temporarily restricted funds have a time or purpose restriction that will eventually be released. A grant to run a summer program is temporarily restricted, once the program runs and the funds are spent appropriately, the restriction is released and the funds move to unrestricted net assets. This release is recorded as a reclassification (a debit to net assets with donor restrictions and a credit to net assets without donor restrictions), not as income.

Permanently restricted funds

Permanently restricted funds (now called 'net assets with donor restrictions - permanent' under ASU 2016-14) maintain their restriction indefinitely. Endowments are the most common example. Only the investment income generated may be spendable, and often only if the donor specifies.

Practical bookkeeping implication

Every incoming donation or grant must be coded on receipt as restricted or unrestricted. When a restricted grant is spent, the expenses need to be tagged to that restriction so you can demonstrate compliance to the funder. When the restriction is fulfilled, record a release of restriction, a debit to net assets with donor restrictions and a credit to net assets without donor restrictions.

The 4 Key Financial Statements Nonprofits Must Produce

- Statement of Financial Position

This is your nonprofit's balance sheet. It shows assets, liabilities, and net assets split between with and without donor restrictions, at a point in time. Donors, foundations, and board members use this to assess the organization's liquidity and financial stability.

- Statement of Activities

This is your income statement equivalent. It shows revenue and expenses for the period, but organized by restriction class (with and without donor restrictions) rather than just as a single profit/loss figure. The bottom line isn't "net income" , it's the change in net assets.

- Statement of Functional Expenses

Required for voluntary health and welfare organizations and recommended for all nonprofits, this statement shows expenses broken down simultaneously by nature (salaries, rent, supplies) and by function (program, management, fundraising). It's the document that reveals how much of every dollar raised goes to the mission vs overhead which is exactly what sophisticated donors and sites like Charity Navigator and GuideStar (now Candid) analyze.

- Statement of Cash Flows

Identical in structure to the for-profit version, operating, investing, and financing activities, but critically important for nonprofits that have significant grant timing mismatches. Receiving a large grant in December and spending it over the following year can create cash flow complexity that the Statement of Activities alone doesn't capture.

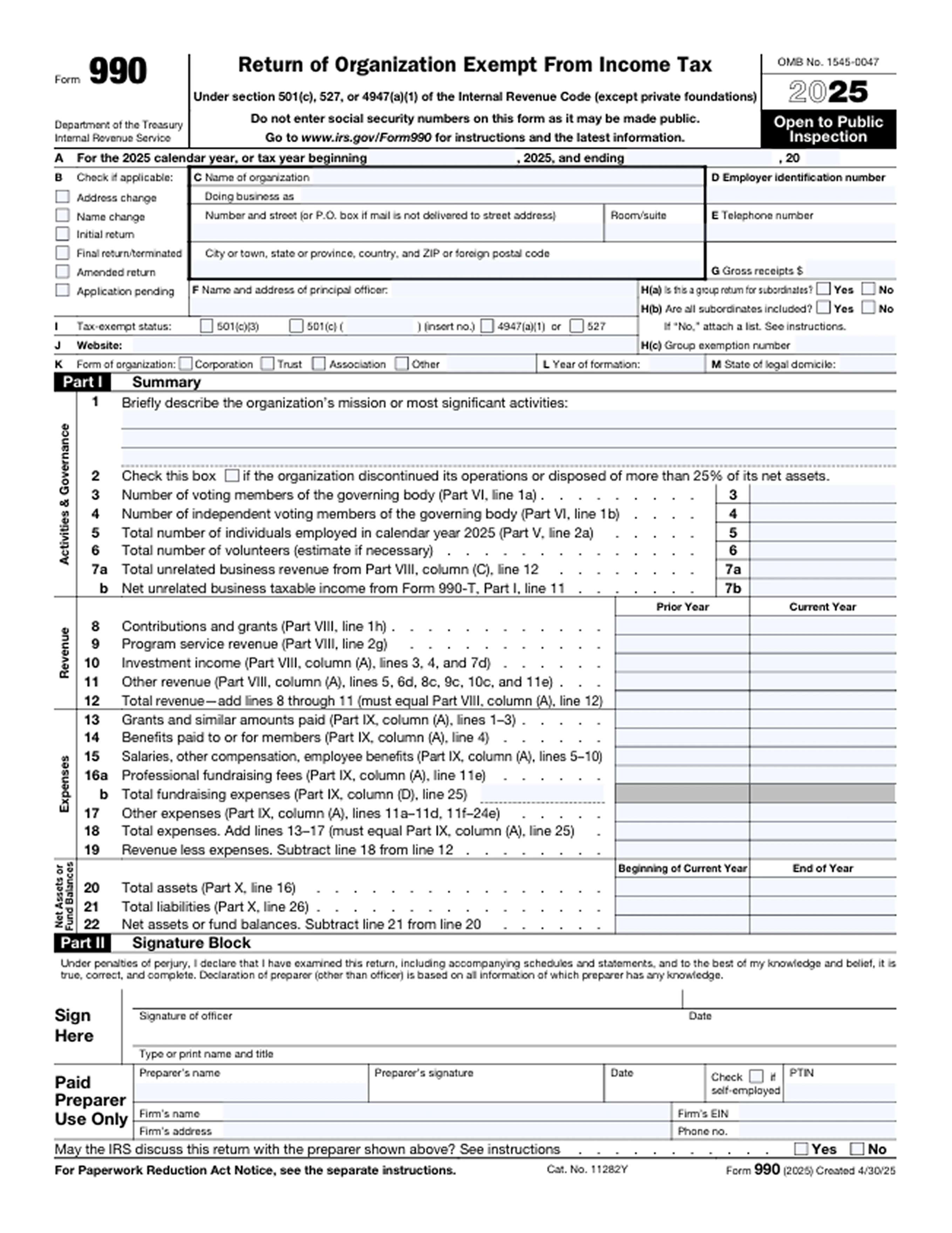

Form 990: The Nonprofit Tax Return

Nonprofits don't pay income tax, but they do file an annual information return with the IRS Form 990. The version you file depends on your gross receipts:

Form 990 is public, anyone can look it up on IRS. This means your revenue, expenses, executive compensation, and program descriptions are visible to every donor, grant officer, and journalist who searches for your organization. Clean, well-organized books that accurately reflect your mission impact aren't just about compliance they're your public financial reputation.

The filing deadline is the 15th day of the 5th month after your fiscal year ends. For December 31 fiscal year end, that's May 15. Automatic 6-month extensions are available, but missing three consecutive years of filing results in automatic revocation of tax-exempt status under the Pension Protection Act a serious consequence that requires a formal reinstatement process to undo.

Tips for preparing your Form 990

- Reconcile your books to your trial balance before starting. Discrepancies between your internal records and Form 990 figures are a common audit trigger.

- Schedule B (Schedule of Contributors) requires listing donors who gave $5,000 or more during the year. Make sure donor records are current and complete.

- Part VII (compensation of officers and key employees) is one of the most-read sections by journalists and watchdog organizations to ensure executive salaries are documented with board approval records.

- Program accomplishment narratives in Part III directly influence grant decisions using specific, measurable outcomes rather than vague mission language.

- If your 990 shows a large variance from the prior year in any category, add a brief explanation in the relevant section to preempt questions from reviewers.

Grant Management and Reporting

Grants are the lifeblood of many nonprofits, and they come with reporting obligations that make bookkeeping accuracy genuinely mission-critical.

Grant tracking requirements:

Most foundation and government grants require a financial report at the end of the grant period showing exactly how the funds were spent, often with receipts or backup documentation. If your books aren't coded to the grant, producing this report means manually reconstructing months of transactions, which is slow, error-prone, and exactly the wrong impression to make on a funder you want to renew.

Best practice: create a separate class or project code for every active grant in your accounting system. Every expense charged to that grant gets tagged. At any point you can run a report showing exactly how much of the grant has been spent, on what, and what remains.

Deferred revenue:

When you receive a grant before you've done the work it funds, that money is deferred revenue, a liability on your balance sheet, not income. As you spend the grant on eligible expenses and fulfill the grant conditions, you recognize it as revenue. This matching principle matters both for accurate financial statements and for grant compliance. You shouldn't recognize the full grant as revenue on day one if the work spans two fiscal years.

In-kind contributions:

Donated goods and services must be recorded at fair market value, both as revenue and as expense. A law firm that provides $5,000 in pro bono legal services should appear on your books as $5,000 in in-kind revenue and $5,000 in professional fees expense. This matters for Form 990 accuracy and for calculating your true program cost. The IRS guidance on in-kind contributions and FASB ASC 958-605 govern how these are recorded.

Payroll and Functional Expense Allocation

Payroll is typically the largest expense in most nonprofits, and it's also the most complex to book correctly because staff members often split their time across programs, administration, and fundraising.

Time tracking and allocation:

If your program director spends 70% of their time on direct program delivery, 20% on administrative work, and 10% on fundraising activities, their salary should be allocated across those three functional categories in those proportions. This isn't optional, FASB and IRS both require functional expense reporting, and allocating all staff costs to program expenses to make your overhead ratio look better is a misrepresentation that auditors and sophisticated funders will identify.

The practical approach: require staff to submit monthly time allocation percentages if exact time tracking isn't feasible. Document the methodology and apply it consistently.

Payroll tax obligations:

Nonprofits are exempt from paying federal income tax, but they are not exempt from payroll taxes. You still owe employer FICA contributions (Social Security and Medicare), must withhold employee FICA and federal income tax, and must file Form 941 quarterly. Some states offer limited payroll tax exemptions for nonprofits, check with your state's department of revenue.

Monthly Bookkeeping Checklist for Nonprofits

Whether you're handling books internally or working with an outsourced bookkeeper, these tasks need to happen every month:

- Record all incoming contributions and grants, coded immediately to the correct restriction class. Don't let unclassified donations accumulate; the longer they sit uncoded, the harder classification becomes.

- Reconcile all bank accounts and credit cards. Every transaction should match a receipt or source document. Unexplained items should be flagged and resolved within the same month they appear.

- Process payroll and allocate staff costs to the correct functional categories. If your allocation percentages changed because a staff member shifted roles, update the split.

- Review restricted fund balances. Are you spending restricted grants at the pace required? Are any grants at risk of under-spending relative to the grant period end date? Under-spending on a restricted grant can sometimes require returning funds or explaining the variance to the funder.

- Prepare a simple monthly financial summary for the executive director and board treasurer, at minimum, a Statement of Activities and bank balance by fund. Boards that see financial information monthly make better decisions than boards that see it quarterly.

- File any payroll tax deposits. The IRS deposit schedule, monthly or semi-weekly depending on your payroll size, must be followed precisely to avoid penalties.

Year-End Close Checklist for Nonprofits

The year-end close is your most critical bookkeeping milestone. Complete these steps before filing Form 990 or presenting final financials to your board:

- Reconcile all bank, investment, and credit card accounts to December 31 statements.

- Review and close all deferred revenue accounts and confirm unspent grant balances are correctly classified as liabilities, not income.

- Process all release-of-restriction journal entries for grants and contributions whose conditions were fulfilled during the year.

- Reconcile in-kind contribution records and ensure all donated goods and services are recorded at fair market value.

- Prepare final payroll allocation percentages and ensure all year-end payroll journal entries are posted.

- Prepare draft financial statements for board review including all four statements, not just the Statement of Activities.

- Pull a functional expense schedule and verify program vs overhead ratios align with board expectations and funder requirements.

- Compile grant files and organize all expense documentation, receipts, and allocation records by grant for upcoming reporting deadlines.

- Confirm Form 990 preparation timeline with your CPA or preparer as the May 15 deadline comes faster than most organizations expect.

Frequently Asked Questions