Summary

Delaware corporations can choose between two franchise tax calculation methods: the Authorized Shares Method (Delaware's default, often resulting in inflated bills) and the Assumed Par Value Capital Method (almost always lower for startups). You are legally allowed to pay whichever is smaller.

- Delaware corporations must file and pay franchise tax by March 1 each year

- LLCs and partnerships pay a flat $300 fee due by June 1, no complex calculation needed

- The Assumed Par Value Capital method can reduce a startup's bill from $85,000+ down to as little as $400

- Delaware does not automatically apply the APVC method, you must select it manually when filing

- Missing the deadline triggers a $200 flat penalty plus 1.5% monthly interest on the unpaid balance

- The Annual Report must be filed at the same time as the franchise tax, with a separate $50 fee

- All filing and payment is handled online at corp.delaware.gov, no paper filings are accepted

If you've incorporated in Delaware or plan to, the annual franchise tax is one obligation you can't afford to overlook. Delaware is home to more than 60% of Fortune 500 companies for good reason: its business-friendly legal environment, Court of Chancery, and flexible corporate statutes. But that incorporation comes with a cost, and understanding exactly how that cost is calculated can save your company thousands of dollars every year.

This guide covers everything you need to know about the Delaware franchise tax: who must pay it, how to calculate it using either IRS-approved method, 2025–2026 due dates, and how to pay online.

What Is the Delaware Franchise Tax?

The Delaware franchise tax is an annual fee charged by the state for the privilege of being incorporated there. It is not a tax on income, meaning you owe it even if your company made no revenue or operated at a loss. It applies to:

- Delaware C-Corporations

- Delaware S-Corporations

- Non-stock for-profit corporations that do not meet exempt status pay a flat $175

- LLCs and partnerships pay a separate flat annual tax (more on this below)

If your corporation was formed in Delaware but operates elsewhere, you still owe this tax. That surprises many founders.

Delaware Franchise Tax: LLC vs. Corporation

Before diving into calculation methods, it helps to understand the difference in how LLCs and corporations are taxed.

- Delaware LLCs and partnerships pay a flat annual tax of $300, due June 1 each year. There is no complex calculation involved; it is a flat fee regardless of revenue or size.

- Delaware corporations (C-Corps and S-Corps) are subject to a more complex franchise tax formula, and this is where most confusion and most savings opportunities lie. Two calculation methods are available, and you get to choose the one that results in a lower tax bill.

The Two Calculation Methods for Delaware Corporations

Method 1: Authorized Shares Method

This is Delaware's default method. The state uses it to calculate your initial franchise tax estimate, and it is the reason so many startups receive shockingly large tax bills in the mail, sometimes in the tens of thousands of dollars.

The formula is based on the number of shares your corporation is authorized to issue:

.webp)

Example

A corporation with 10,005 authorized shares pays $335 ($250 + $85).

The Problem

Most startups authorize millions of shares at formation. Under this method, that can translate into a franchise tax bill of $85,000 or more even for a pre-revenue company.

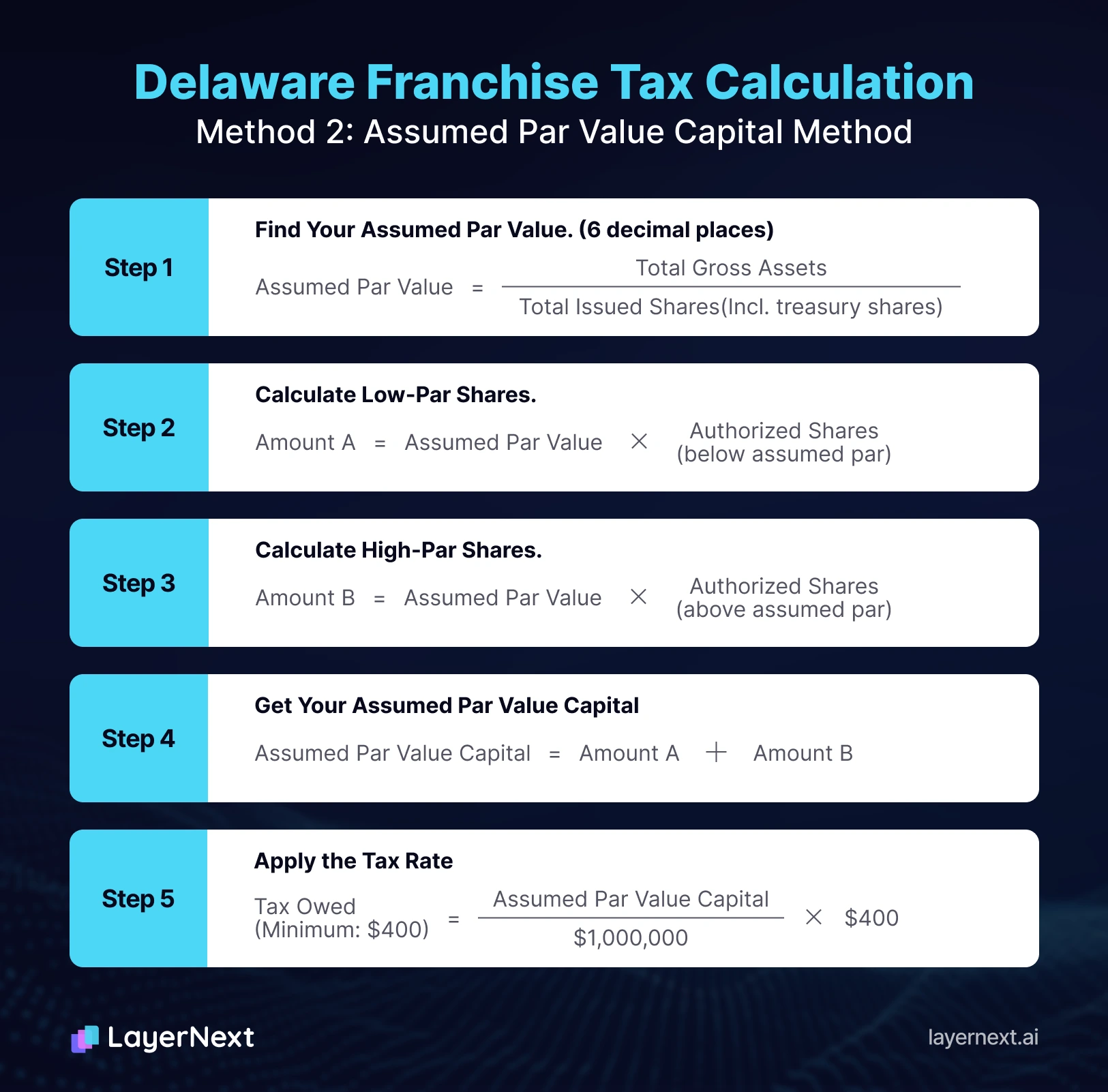

Method 2: Assumed Par Value Capital Method

The Assumed Par Value Capital (APVC) method almost always produces a significantly lower tax bill for startups and growing companies. It calculates the tax based on your company's actual issued shares and total gross assets, specifically those total assets reported on U.S. Form 1120, Schedule L of your Federal Return for the fiscal year ending December 31.

Here is how it works:

Step 1: Divide your total gross assets by your total issued shares (including treasury shares) to get the assumed par value per share. Carry this figure to 6 decimal places.

Step 2: For authorized shares with a par value below the assumed par, multiply the assumed par by the number of those shares.

Step 3: For authorized shares with a par value above the assumed par, multiply the number of those shares by their actual par value.

Step 4: Add the results of Steps 2 and 3 together. This total is your assumed par value capital.

Step 5: Apply the tax rate of $400 per $1,000,000 of assumed par value capital (or fraction thereof). If your assumed par value capital is under $1,000,000, divide it by $1,000,000 and multiply by $400. The minimum tax under this method is $400.

Example

Gross assets: $1,000,000

Issued shares: 485,000

Authorized shares: 1,000,000 shares at $1.00 par value and 250,000 shares at $5.00 par value

Assumed par value = $1,000,000 / 485,000 = $2.061856 per share

Shares with par value below assumed par: 1,000,000 x $2.061856 = $2,061,856

Shares with par value above assumed par: 250,000 x $5.00 = $1,250,000

Assumed par value capital = $2,061,856 + $1,250,000 = $3,311,856

Tax = 4 x $400 = $1,600

Compared to potentially $75,000 or more under the Authorized Shares Method, the savings are substantial. You should always calculate your tax under both methods and pay the lower amount.

Large Corporate Filers

Not all corporations use the standard methods. A Large Corporate Filer is defined as a corporation that has a class or series of stock listed on a national securities exchange and reported either consolidated annual gross revenues of at least $750 million or consolidated assets of at least $750 million, combined with both revenues and assets of at least $250 million. These corporations pay a fixed franchise tax of $250,000 regardless of which standard method would otherwise apply.

How to Calculate Your Delaware Franchise Tax

- Pull your balance sheet and federal return.

You will need total gross assets from Form 1120, Schedule L, total issued shares (including treasury shares), and total authorized shares as of December 31 of the tax year. - Calculate under both methods using Delaware's online calculator at corp.delaware.gov or the formulas above.

- Choose the lower result. You are legally permitted to use whichever method is in your favor.

- File your Annual Report and pay the tax together.

The Delaware Division of Corporations does not automatically apply the APVC method. You must specifically request it when filing. If you file online, there is a field to input the required data and select the method.

Delaware Franchise Tax Due Dates (2025 and 2026)

Missing the deadline triggers penalties and interest, so mark these dates clearly:

For the 2026 tax year (covering calendar year 2025), the corporation deadline was March 1, 2026. If you missed that deadline, the $200 penalty and 1.5% monthly interest are already accruing as of today.

Important: Corporations owing $5,000 or more in franchise tax must make estimated payments in installments rather than a single payment. The schedule is:

- 40% due June 1

- 20% due September 1

- 20% due December 1

- Remaining balance due March 1

The Annual Report carries a separate $50 filing fee that is not included in the franchise tax amount.

Step-by-Step Guide to Filing Delaware Franchise Tax Online

Step 1: Identify your entity type.

Confirm whether your entity is a corporation (C-Corp or S-Corp) or an LLC. LLCs skip the steps below and simply pay a flat $300 by June 1.

Step 2: Gather your financial data.

Pull your balance sheet as of December 31 of the tax year. You will need three figures: total gross assets, total issued shares, and total authorized shares.

Step 3: Calculate under the Authorized Shares Method.

Use the tiered table in this guide to find your tax based solely on how many shares your corporation is authorized to issue.

Step 4: Calculate under the Assumed Par Value Capital Method.

Divide gross assets by issued shares to get the assumed par value. Multiply that by authorized shares to get assumed par value capital. Divide by $1,000,000 and multiply by $400. The minimum under this method is $400.

Step 5: Choose the lower result.

You are legally permitted to pay whichever method produces the smaller bill. For most startups with large authorized share counts, the APVC method wins by a wide margin.

Step 6: Visit the Delaware Division of Corporations portal.

Go to corp.delaware.gov and select "Pay Taxes / File Annual Report."

Step 7: Enter your Entity File Number.

This is printed on your certificate of incorporation and is required to look up your entity in the system.

Step 8: Input your financial data if using APVC.

There is a specific field during the online filing process to enter gross assets, issued shares, and authorized shares so the system can apply the APVC method. It will not apply this method automatically.

Step 9: File your Annual Report simultaneously.

The Annual Report must be submitted at the same time as the franchise tax payment. A separate $50 filing fee applies.

Step 10: Submit payment and save your confirmation.

Delaware accepts credit card or electronic check. Save or screenshot your payment confirmation for your records and future due diligence.

The entire process typically takes under 15 minutes. Delaware does not accept paper filings for franchise tax payments.

Delaware Franchise Tax Minimums and Exemptions

Minimum tax under the Authorized Shares Method: $175

Minimum tax under the APVC Method: $400

Maximum tax for standard corporations: $200,000

Maximum tax for Large Corporate Filers: $250,000

Non-stock for-profit corporations not meeting exempt criteria: flat $175

Nonprofit corporations with 501(c) IRS status: exempt from franchise tax, but must file an Annual Report with a $25 fee

Common Mistakes to Avoid

Relying on Delaware's default estimate. The state sends estimated tax bills using the Authorized Shares Method. These estimates are almost always far higher than what you actually owe. Do not pay the estimate without running the APVC calculation first.

Using gross assets from the wrong source. Total gross assets must come from Form 1120, Schedule L of your federal return, not from an internal balance sheet or accounting software export that may use different classifications.

Forgetting the estimated payment schedule. If your franchise tax liability is $5,000 or more, you are required to make quarterly estimated payments throughout the year, not a single payment on March 1.

Forgetting the Annual Report. The $50 Annual Report fee is separate from the franchise tax and must be filed simultaneously. Missing it creates a compliance gap that can affect fundraising due diligence.

Confusing tax year and payment year. Delaware franchise tax is paid in arrears. The March 1, 2026 deadline covers the fiscal year ending December 31, 2025.

Not accounting for multiple entity types. If you operate both a Delaware LLC and a Delaware corporation, each entity owes its own separate tax.

Mishandling mid-year stock amendments. If you filed an amendment changing your stock or par value during the year, you must provide issued shares and gross assets within 30 days of the amendment for each portion of the year. The tax is then prorated based on the number of days each share structure was in effect.

Streamline Compliance with the Right Tools

Managing annual compliance across multiple entities tracking due dates, storing balance sheet data for APVC calculations, and archiving filed reports, is exactly the kind of structured workflow that benefits from modern tooling.

LayerNext is an AI-powered platform that helps businesses organize, manage, and retrieve critical documents and workflows. Whether you're a founder managing a single Delaware entity or a finance team handling compliance across a portfolio of companies, LayerNext.ai can help you centralize the documents you need at tax time from balance sheets to prior-year filings so nothing falls through the cracks when deadlines approach.

Frequently Asked Questions