Summary

GST/HST compliance comes down to four things: knowing when to register, charging the right rate based on where your customer is located, claiming input tax credits accurately, and filing on time. Miss any of these and CRA's penalties compound fast.

- Registration threshold: You must register once taxable revenue crosses $30,000 in four consecutive calendar quarters or a single quarter. You have 29 days to register after crossing it.

- Place of supply: The rate you charge depends on your customer's location, not yours. An Ontario business invoicing an Alberta client charges 5% GST, not 13% HST.

- Input tax credits: ITCs let you recover GST/HST paid on business expenses. Meals and entertainment are capped at 50%. Personal-use portions of mixed expenses do not qualify.

- Annual filer trap: Your GST/HST balance is due April 30, even if your return itself is not due until three months after your fiscal year-end. This mismatch causes most annual-filer penalties.

- Quick Method: Service businesses with low input costs often remit less tax under the Quick Method than under the regular method. Run the comparison before electing.

Canada Revenue Agency assessed over $1 billion in GST/HST penalties and interest in a recent year. The vast majority came from small businesses, not because they were trying to avoid taxes, but because they missed a deadline, miscalculated a remittance, or didn't realize they needed to register in the first place.

If you're a new business owner, freelancer, sole proprietor, or recently incorporated, this guide is for you. We'll walk through everything: what GST/HST is, when you need to register, how often to file, how to claim input tax credits, what penalties look like, and how to keep yourself audit-ready. No jargon, no fluff, just a practical roadmap to staying compliant with the CRA.

As of 2024, there are over 1.2 million GST/HST registrants in Canada. Most of them figured this out the hard way. You don't have to.

What Is GST/HST and How Does It Work?

GST stands for Goods and Services Tax, a federal tax of 5% that applies to most goods and services sold in Canada. HST, the Harmonized Sales Tax, combines the federal GST with a provincial sales tax into a single rate. It applies in provinces that have agreed to harmonize their tax system with the federal government: Ontario, Nova Scotia, New Brunswick, Newfoundland & Labrador, and Prince Edward Island.

In provinces that haven't harmonized, British Columbia, Saskatchewan, Manitoba, and Quebec businesses collect GST federally and a separate provincial sales tax (PST or QST) provincially. Alberta, Yukon, the Northwest Territories, and Nunavut have no provincial sales tax at all, so only the 5% GST applies.

The ITC system is what makes GST/HST work as a business.

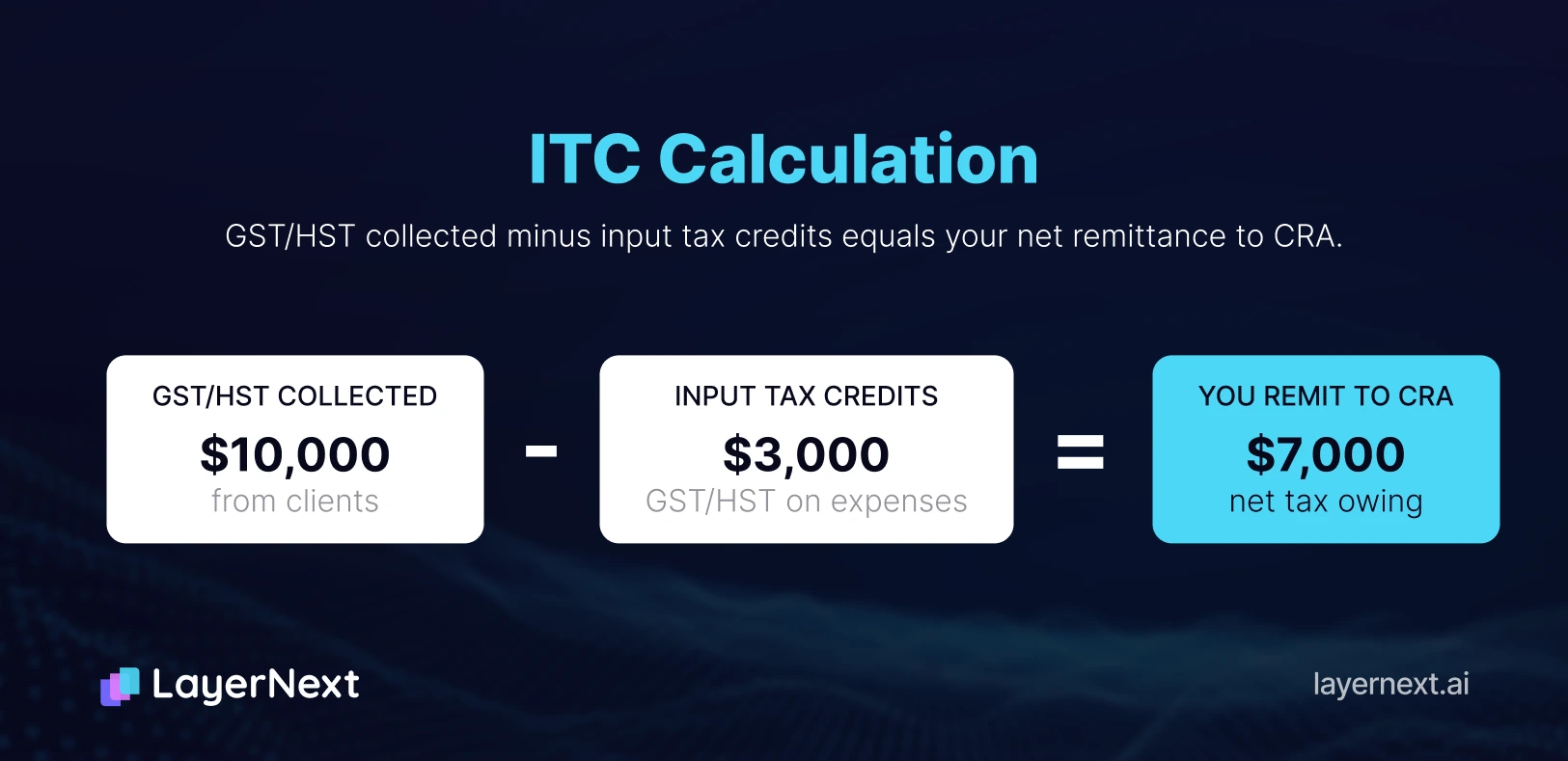

Here's the basic mechanic: you collect GST/HST from your customers on taxable sales. You pay GST/HST on your own business purchases. The GST/HST you paid on business expenses is called an Input Tax Credit (ITC). When you file your return, you subtract your ITCs from the GST/HST you collected and remit the difference to the CRA.

Simple example

Say you collected $10,000 in GST/HST from clients during the quarter. You paid $3,000 in GST/HST on rent, software, and supplies. Your net tax owing is $7,000, that's what you remit to CRA.

If your ITCs exceed what you collected (common for businesses with high startup costs), CRA owes you a refund.

HST Rates by Province (2026)

The rate you charge depends not on where your business is located, but on where your customer is. This is called the place of supply rule, and it matters especially if you sell to customers across multiple provinces.

.webp)

A practical example of place of supply: An Ontario-based consultant invoices a client in Alberta. They charge 5% GST, not 13% HST, because the service is supplied where the customer is located (Alberta), not where the business operates.

For most services, place of supply is where the customer is. For physical goods, it's generally where the goods are delivered. For digital services, the rules follow the customer's location. If you sell across provinces regularly, it's worth reviewing the CRA's place of supply rules or consulting an accountant, because getting this wrong means charging the wrong rate, which creates both a compliance issue and a customer experience problem.

Do You Need to Register for GST/HST?

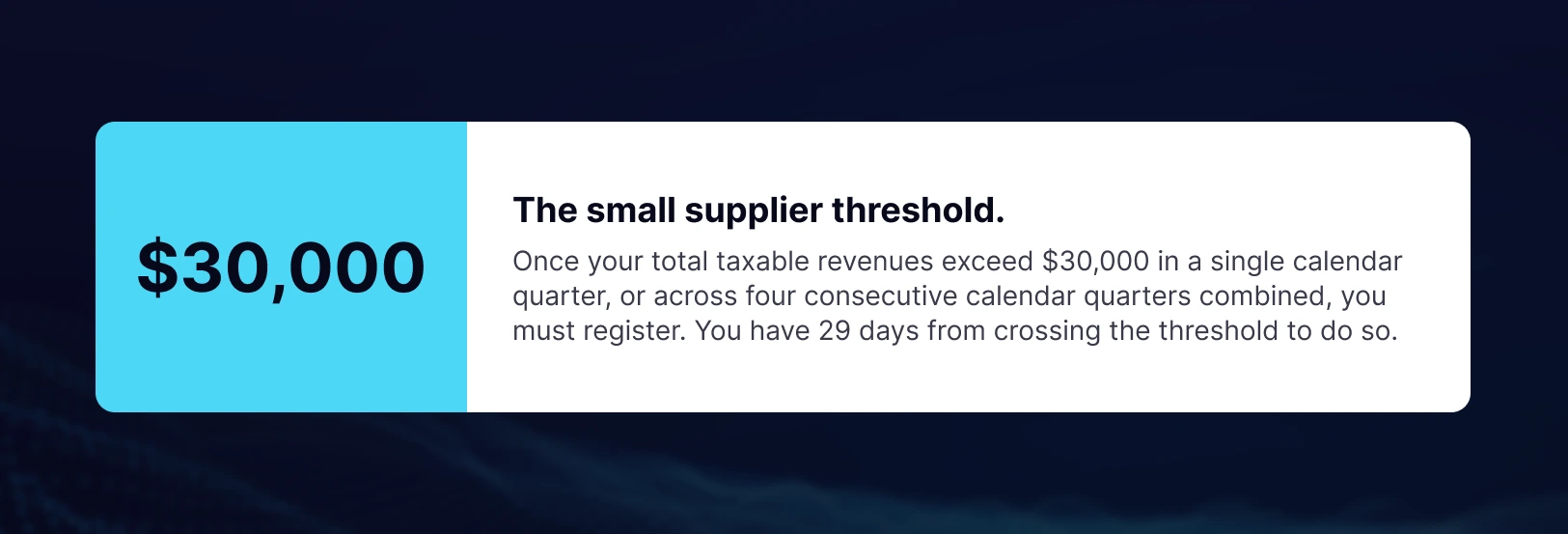

The $30,000 Small Supplier Threshold

Most businesses aren't required to register for GST/HST until their taxable revenues exceed $30,000. Specifically, you must register once your total taxable revenues exceed $30,000 in a single calendar quarter, or in four consecutive calendar quarters combined.

Once you cross that threshold, you have 29 days to register.

A few important points about how this threshold works:

The $30,000 applies to taxable supplies, goods or services on which GST/HST would be charged. It excludes exempt supplies (more on those below). It also applies to associated businesses, if you own multiple businesses that are closely related, their revenues may be combined for threshold purposes.

Who Must Register Regardless of Revenue

Some businesses must register from the first dollar, no matter how small:

- Taxi and ride-sharing drivers (Uber, Lyft, etc.)

- Non-resident businesses selling digital services or physical goods to Canadian consumers

- Non-resident platform operators under the digital economy rules

Voluntary Registration: Why It Often Makes Sense

If your revenue is below $30,000, you're not required to register, but you can choose to. This is worth considering seriously if you have significant startup expenses. As an unregistered small supplier, you pay GST/HST on your business purchases and can't recover it. Once registered, you can claim ITCs on those costs.

If your clients are other businesses (B2B), they can claim back whatever GST/HST you charge them anyway, so voluntary registration rarely creates friction with customers and directly benefits your cash flow.

Who Is Exempt from Registering

Businesses that supply only exempt supplies do not need to register and cannot claim ITCs. Exempt supplies include residential rent, most health care services, educational services, and financial services. If you're in one of these sectors, confirm your status with an accountant the line between exempt and taxable can be nuanced.

How to Register for a GST/HST Account

Registration is straightforward and can be done in a few ways:

Online via CRA My Business Account is the fastest option. If you don't already have a My Business Account, you'll need to create one using your SIN and a recent tax return for identity verification. The registration itself takes only a few minutes once you're logged in.

By phone at 1-800-959-5525 during business hours. A CRA agent will walk you through the process.

By mail using Form RC1 (Request for a Business Number). This is the slowest option and not recommended if you need to start collecting GST/HST soon.

Once registered, CRA will issue you a Business Number (BN), a 9-digit number that identifies your business, along with an RT0001 suffix that identifies your GST/HST account specifically. This number must appear on every invoice you issue.

Choosing your effective registration date matters. You can typically choose a date that aligns with when you crossed the $30,000 threshold, or an earlier date if you want to recover ITCs on prior purchases (particularly relevant for capital property held at the time of registration). In some cases, retroactive registration going back up to 30 days is permitted.

What to do immediately after registration: update all your invoice templates to include your GST/HST registration number and the amount of tax charged, and start collecting the appropriate rate from customers on all taxable supplies.

Incorporated businesses vs. sole proprietors

A common misconception: incorporating your business does not exempt you from GST/HST. The $30,000 registration threshold applies equally to corporations, sole proprietors, and partnerships. The legal structure of your business has no bearing on your GST/HST obligations.

What changes with incorporation is the identity of the registrant. A sole proprietor registers using their personal SIN and receives a BN tied to their individual business. A corporation registers as a separate legal entity with its own BN. If you incorporate an existing sole proprietorship that was already registered, you'll need to register the corporation separately and close the sole proprietor account.

TRANSITIONING FROM SOLE PROPRIETOR TO CORPORATION

If you incorporated and your sole proprietorship had accumulated ITCs or outstanding remittances, those do not transfer automatically. File a final GST/HST return under the sole proprietor account, then begin fresh with the corporate registration. Missing this step is a common source of CRA compliance notices.

GST/HST Reporting Periods : How Often Do You File?

CRA assigns a filing frequency based on your annual taxable revenues:

Most small businesses start as annual filers. That's convenient administratively, but it has a cash flow implication: you're collecting GST/HST from customers all year and only remitting once. Some business owners treat that accumulated balance as working capital which creates a nasty surprise at filing time if the money has been spent.

You can elect to file more frequently than your assigned period. If quarterly or monthly filing helps you stay on top of cash flow and avoid large year-end remittances, you can request a change through CRA My Business Account.

The December 31 fiscal year-end exception: Annual filers with a fiscal year ending December 31 have until June 15 to file their return, but any balance owing is still due by April 30. This is a common source of confusion, and penalties for businesses that wait until June 15 to pay.

What Goes Into a GST/HST Return

Filing a GST/HST return requires four core numbers:

1. Total sales and other revenue - the total value of all taxable supplies you made during the reporting period, before tax.

2. GST/HST collected (or collectible) - the total GST/HST you charged customers. Note that GST/HST is collectible when the invoice is issued, not necessarily when you receive payment unless you're using the cash method (available to businesses with revenues under $1.5 million on election).

3. Input Tax Credits (ITCs) - the GST/HST you paid on eligible business expenses during the period. You must have supporting documentation (receipts, invoices) for every ITC you claim.

4. Net tax owing -GST/HST collected minus ITCs. This is what you remit. If it's negative, CRA owes you a refund.

Common ITC-Eligible Business Expenses

- Office rent and utilities

- Business equipment and technology

- Software subscriptions used for business

- Professional services (accountant, lawyer, consultant)

- Advertising and marketing costs

- Business vehicle expenses (subject to restrictions on personal-use portions)

- Meals and entertainment — only 50% of the GST/HST paid is claimable here

What Is NOT Eligible for ITCs

- Personal expenses or personal portions of mixed-use expenses

- Expenses related to exempt supplies

- Employee wages, salaries, and most payroll-related costs

- Capital property used less than 10% for commercial activity

One common mistake: claiming ITCs on expenses that have both personal and business use without properly prorating them. If your cell phone is 60% business and 40% personal, only 60% of the GST/HST paid qualifies as an ITC.

ITC CLAIM DEADLINE

You have four years from the filing due date of the return in which the ITC first became claimable to include it in a return. After that, the credit is lost. For businesses that have missed ITCs in prior years, it's worth reviewing past periods before the window closes.

How to File Your GST/HST Return

Filing Methods

- NETFILE via CRA My Business Account is the recommended method for most businesses. It's fast, provides instant confirmation, and processes refunds more quickly than any other method.

- TELEFILE (1-800-959-2038) allows eligible filers to file by phone using a touchtone keypad. It works but is limited in flexibility.

- EDI (Electronic Data Interchange) is used by large businesses that file through financial institutions or third-party software. Not relevant for most small businesses.

- Paper filing (Form GST34) is available but not recommended. It's the slowest option, delays refunds significantly, and creates more room for data entry errors.

Step-by-Step: Filing via My Business Account

- Log in to your CRA My Business Account at canada.ca

- Navigate to your GST/HST account (listed under your RT0001 program account)

- Select the reporting period you're filing for

- Enter your total sales and other revenue

- Enter the total GST/HST collected or collectible

- Enter your total ITCs

- Review the calculated net tax

- Submit the return

- Save your confirmation number (this is your proof of filing)

The whole process takes 5–10 minutes if your books are in order. The bottleneck is never the filing itself, it's having accurate numbers ready when you sit down to file.

How to Pay Your GST/HST Balance

Payment Methods

- Online banking is the most common and convenient method. Add "CRA (Revenue) GST/HST" as a payee through your business bank account, use your Business Number as the account number, and pay like any other bill.

- CRA My Payment at canada.ca/cra-my-payment allows payment via Visa Debit or Mastercard Debit directly. Note that credit cards are not accepted for CRA payments.

- Wire transfer is available for very large payments (over $25 million) coordinated through financial institutions.

- In person at a financial institution with a remittance voucher. You can get your remittance voucher through My Business Account.

- Cheque payable to the Receiver General for Canada, mailed to CRA. Technically works but slow, and mail delays don't excuse late payment.

INSTALMENT PAYMENTS FOR ANNUAL FILERS

Annual filers whose net tax exceeds $3,000 in the current or previous year are required to make quarterly instalment payments. CRA will notify you, but it's worth knowing in advance if your business is growing and your remittances are increasing.

Key Payment Deadlines

Monthly and quarterly filers: payment is due on the same day as your return, one month after the end of each reporting period.

Annual filers: payment is due April 30, even though your return may not be due until three months after your fiscal year-end (or June 15 for December 31 year-ends). This mismatch trips up a lot of annual filers.

Instalment payments: Annual filers whose net tax exceeds $3,000 in the current or previous year are required to make quarterly installment payments. CRA will notify you, but it's worth knowing if your business is growing and your remittances are increasing.

Penalties, Interest, and What Happens If You Miss a Deadline

Late Filing Penalty

The standard late filing penalty is 1% of the balance owing, plus 0.25% for each complete month the return is late, up to a maximum of 12 months, so up to 4% total. If you've been assessed a late filing penalty in the previous three years, the penalty increases.

Arrears Interest

CRA charges compound daily interest on any overdue balance. The prescribed interest rate changes quarterly and is generally set at the Bank of Canada rate plus a few percentage points. Even a modest balance left unpaid for several months can accumulate meaningful interest charges.

Failure to Register Penalty

If CRA determines you were required to register and didn't, they can assess GST/HST going all the way back to the date you should have registered, plus penalties and interest on everything you should have collected and remitted. This is one of the more expensive mistakes a small business can make.

What to Do If You Can't Pay

- File on time even if you can't pay. The late filing penalty is separate from arrears interest. Filing on time eliminates the filing penalty, even if you carry an unpaid balance. Then contact CRA to arrange a payment plan, they do work with businesses in financial difficulty.

- CRA's Voluntary Disclosures Program (VDP) is available if you've never filed, filed incorrectly, or failed to report income. Coming forward proactively through VDP typically results in penalty relief and, in some cases, interest relief as well. It's worth considering if you're behind on filing and worried about the consequences of CRA finding it first.

The GST/HST Quick Method: rates, eligibility, and how to elect

If tracking every single ITC sounds like a lot of work for your business, the Quick Method is worth knowing about.

What It Is

Instead of tracking individual ITCs on all your business expenses, the Quick Method lets you remit a fixed percentage of your gross sales (including GST/HST collected) to CRA. The rates are calibrated so that the percentage accounts for a reasonable average ITC claim, you give up precision in exchange for simplicity.

Who Qualifies

Businesses with annual taxable supplies of $400,000 or less (including GST/HST) can elect the Quick Method. However, certain professions are excluded regardless of revenue: accountants, lawyers, financial consultants, actuaries, bookkeepers, and similar advisory services cannot use the Quick Method.

Remittance Rates (2026)

There's also a 1% credit on the first $30,000 of eligible supplies each year, which further reduces your remittance.

When the Quick Method Saves You Money

For service businesses with relatively low ITC-eligible expenses, a freelancer, a consultant, a coach, the Quick Method often results in lower remittances than the regular method, because the remittance rate assumes more ITCs than the business actually incurs.

For businesses with high input costs (manufacturing, retail with significant inventory), the regular method typically produces lower remittances because actual ITCs are larger.

The math is worth running before you elect. You can switch methods annually by filing Form GST74 with CRA.

GST/HST for Special Business Situations

E-Commerce and Online Sellers

If you sell physical goods to Canadian customers, GST/HST applies based on where the goods are delivered. If you sell digital services (software, subscriptions, downloads) to Canadian consumers, GST/HST applies even if your business is based outside Canada, this is the "Netflix rule" that CRA extended to require foreign digital platforms to register and collect.

If you sell through platforms like Amazon, Shopify, or Etsy, the platform may collect and remit GST/HST on your behalf for certain transactions, but this depends on the platform and the nature of the sale. Don't assume the platform is handling it. Know your own obligations independently.

Drop shipping across provinces introduces a place of supply complexity. If a customer in Nova Scotia orders from your Ontario business and the goods ship from a British Columbia warehouse, determining the correct rate requires careful analysis of the transaction structure.

Freelancers and Self-Employed Professionals

Once you cross $30,000 mid-year, you must register within 29 days and start charging GST/HST from that point forward, not retroactively. Keep a running total of your revenues through the year so you're not caught off guard.

For home office expenses, you can claim ITCs on the business-use portion of home office costs if you are self-employed and the home is your principal place of business. Keep consistent records of your business-use percentage.

When invoicing clients in other provinces, remember to apply the rate for the client's location, not yours.

Real Estate

New residential construction is generally subject to GST/HST, though purchasers may qualify for the New Housing Rebate, which partially offsets the tax on homes under a certain value threshold.

Commercial real estate transactions are generally taxable, and GST/HST applies on the sale price. Residential rental income, on the other hand, is generally exempt from GST/HST landlords don't charge it and can't claim ITCs on related expenses.

Non-Profits and Charities

Public service bodies, including charities and qualifying non-profit organizations, have a higher registration threshold of $250,000 in annual revenues rather than the standard $30,000. Many also qualify for special GST/HST rebates that partially recover tax paid on expenses, even when they can't claim full ITCs.

Recordkeeping Requirements for GST/HST

CRA requires you to retain all GST/HST records for six years from the end of the last tax year they relate to. This is not optional, inadequate records during an audit can result in ITCs being denied even if the underlying expenses were legitimate.

What to Keep

Every sales invoice you issued, every purchase receipt you're using to support an ITC claim, your filed GST/HST returns with confirmation numbers, bank statements, and any reconciliation records that tie your returns back to your books.

What a Valid GST/HST Invoice Must Include

If you're issuing invoices that don't meet these requirements, the customers receiving them may be unable to claim ITCs, which creates friction in B2B relationships and reflects poorly on your business.

Storing records digitally is acceptable to CRA, provided the electronic records are accessible, complete, and can be produced in a readable format on request. Cloud-based accounting software with document attachment capabilities handles this well.

How LayerNext Supports Your GST/HST Compliance

GST/HST compliance is fundamentally a bookkeeping problem. If your books are accurate and current, filing is straightforward. If your books are messy, filing becomes stressful, time-consuming, and prone to error.

LayerNext is built specifically for Canadian small businesses, and GST/HST tracking is central to how it works. It automatically categorizes transactions and separates GST/HST collected from your revenue, so you're never manually sorting through bank statements at filing time. It tracks ITCs on eligible expenses in real time, flagging the ones that qualify and applying the correct rules (like the 50% meal and entertainment limitation) so your ITC claims are accurate without manual calculation.

Before each filing period, LayerNext generates clean reports that map directly to the lines on your GST/HST return, total sales, GST/HST collected, total ITCs, net tax. For quarterly and annual filers especially, having those numbers ready instantly rather than reconstructing them from scratch is a meaningful time saving.

LayerNext also syncs with QuickBooks, so if you're already using QuickBooks for your books, your GST/HST balances stay current without double entry. And because your books are organized year-round, there's no year-end scramble to get everything in order before a deadline.

Frequently Asked Questions

Conclusion

GST/HST compliance isn't complicated once you understand the core mechanics: know when you need to register, understand the ITC system, file on time for every period (even nil returns), and keep clean records.

The two mistakes that get most small businesses into trouble are missing the $30,000 threshold and failing to file nil returns after they're registered. Both are easily avoidable with a basic system in place.

Everything else, calculating the right rate, claiming ITCs accurately, choosing between the regular method and the Quick Method becomes much easier when your books are current. That's the real foundation of stress-free GST/HST filing: not scrambling to reconstruct a year's worth of transactions two weeks before a deadline, but having accurate, organized records all year long.