.webp)

Quarterly estimated taxes are advance payments made to the IRS four times per year on income not subject to withholding. Payment deadlines are April 15, June 15, September 15, and January 15. You need to pay if you expect to owe $1,000 or more in federal taxes and your withholding won't cover it.

If you're an entrepreneur, freelancer, or small business owner, quarterly estimated taxes can feel like one of the most confusing responsibilities that comes with earning income outside a traditional paycheck. Unlike employees, no one withholds taxes from your business income for you. That means you're responsible for estimating how much tax you owe and paying it to the IRS throughout the year. When that doesn't happen correctly, penalties, interest, and cash-flow stress can follow.

This comprehensive guide explains what quarterly estimated taxes are, who needs to pay them, how to calculate payments using Form 1040-ES, when payments are due, and what to do if things don't go exactly as planned all in straightforward language.

What Are Quarterly Estimated Taxes?

Quarterly estimated taxes are advance payments you make to the IRS on income that isn't subject to automatic withholding.

The U.S. tax system operates on a pay-as-you-go basis. Instead of waiting until April to collect everything at once, the IRS expects taxes to be paid as income is earned throughout the year.

Estimated taxes generally include:

- Federal income tax

- Self-employment tax (Social Security and Medicare)

- Other applicable federal taxes, depending on your situation

To help individuals calculate and submit these payments, the IRS provides Form 1040-ES.

Official IRS overview of Form 1040-ES: https://www.irs.gov/forms-pubs/about-form-1040-es

Who Needs to File Form 1040-ES in 2026?

You generally need to make quarterly estimated tax payments if:

- You expect to owe $1,000 or more in federal tax when you file your return, and

- Your withholding and refundable credits won't cover that amount

This often applies to:

- Freelancers and independent contractors

- Sole proprietors

- LLC members

- Partners in partnerships

- S-corporation shareholders

- Individuals earning rental, interest, or investment income without withholding

- Gig economy workers (Uber, DoorDash, Upwork, etc.)

Who Doesn't Need to Pay Estimated Taxes?

You may not need to pay estimated taxes if:

- You had no tax liability last year, and

- You were a U.S. citizen or resident for the entire year

IRS estimated tax guidance: https://www.irs.gov/businesses/small-businesses-self-employed/estimated-taxes

Understanding Form 1040-ES: What Is It and How Is It Used?

Form 1040-ES is not a tax return, and it isn't filed once a year like Form 1040.

Instead, it includes:

- A worksheet to estimate your total tax for the year

- Instructions for calculating quarterly payments

- Payment vouchers if you choose to mail payments

The worksheet helps you estimate what you owe. If you pay electronically (which is recommended), you don't submit the form itself you simply keep it for your records.

Download Form 1040-ES (PDF): https://www.irs.gov/pub/irs-pdf/f1040es.pdf

How to Calculate Your Quarterly Estimated Tax Payments: 5-Step Process

Accurate estimates depend on having a clear picture of your income and expenses. The process itself is straightforward once you understand the components.

Step 1: Estimate Your Annual Income

Include all income that isn't subject to withholding, such as:

- Business or freelance income

- Consulting or contract revenue

- Rental income

- Interest and dividends

- Capital gains

- Side hustle income

Pro tip: If your income fluctuates, use year-to-date figures and a reasonable projection for the rest of the year. It's better to slightly overestimate than underestimate.

Step 2: Subtract Deductions and Credits

Common deductions for self-employed individuals include:

- Ordinary and necessary business expenses (office supplies, software, equipment)

- Home office deduction

- Retirement contributions (SEP-IRA, Solo 401(k))

- Health insurance premiums (for eligible self-employed individuals)

- Qualified Business Income (QBI) deduction (up to 20% of qualified income)

- Business mileage or actual vehicle expenses

This helps determine your taxable income rather than just gross revenue.

Step 3: Account for Self-Employment Tax

If you're self-employed, you'll typically owe self-employment tax, which covers Social Security and Medicare. For 2026, the self-employment tax rate is 15.3% (12.4% for Social Security + 2.9% for Medicare).

This tax is calculated separately from income tax and is often underestimated by first-time business owners. Remember: you can deduct half of your self-employment tax as an adjustment to income.

IRS self-employment tax information: https://www.irs.gov/businesses/small-businesses-self-employed/self-employed-individuals-tax-center

Step 4: Use Safe Harbor Rules to Reduce Penalty Risk

The IRS allows safe harbor rules that can help you avoid underpayment penalties even if your estimates aren't exact.

In most cases, you avoid penalties if you pay:

- At least 90% of your current year's tax, or

- 100% of last year's tax (110% if your adjusted gross income was over $150,000, or $75,000 if married filing separately)

Safe harbor explanation: https://www.paychex.com/articles/payroll-taxes/quarterly-taxes

Example: If your 2025 tax liability was $20,000, paying at least $20,000 in estimated taxes for 2026 (in four equal installments of $5,000) protects you from penalties—even if you end up owing $25,000 when you file.

Step 5: Divide the Total Into Quarterly Payments

Once you estimate your total annual tax, divide it into four equal payments. Revisit this calculation during the year if income or expenses change significantly.

Helpful calculation walkthrough: https://turbotax.intuit.com/tax-tips/self-employment-taxes/a-guide-to-paying-quarterly-taxes/L6p8C53xQ

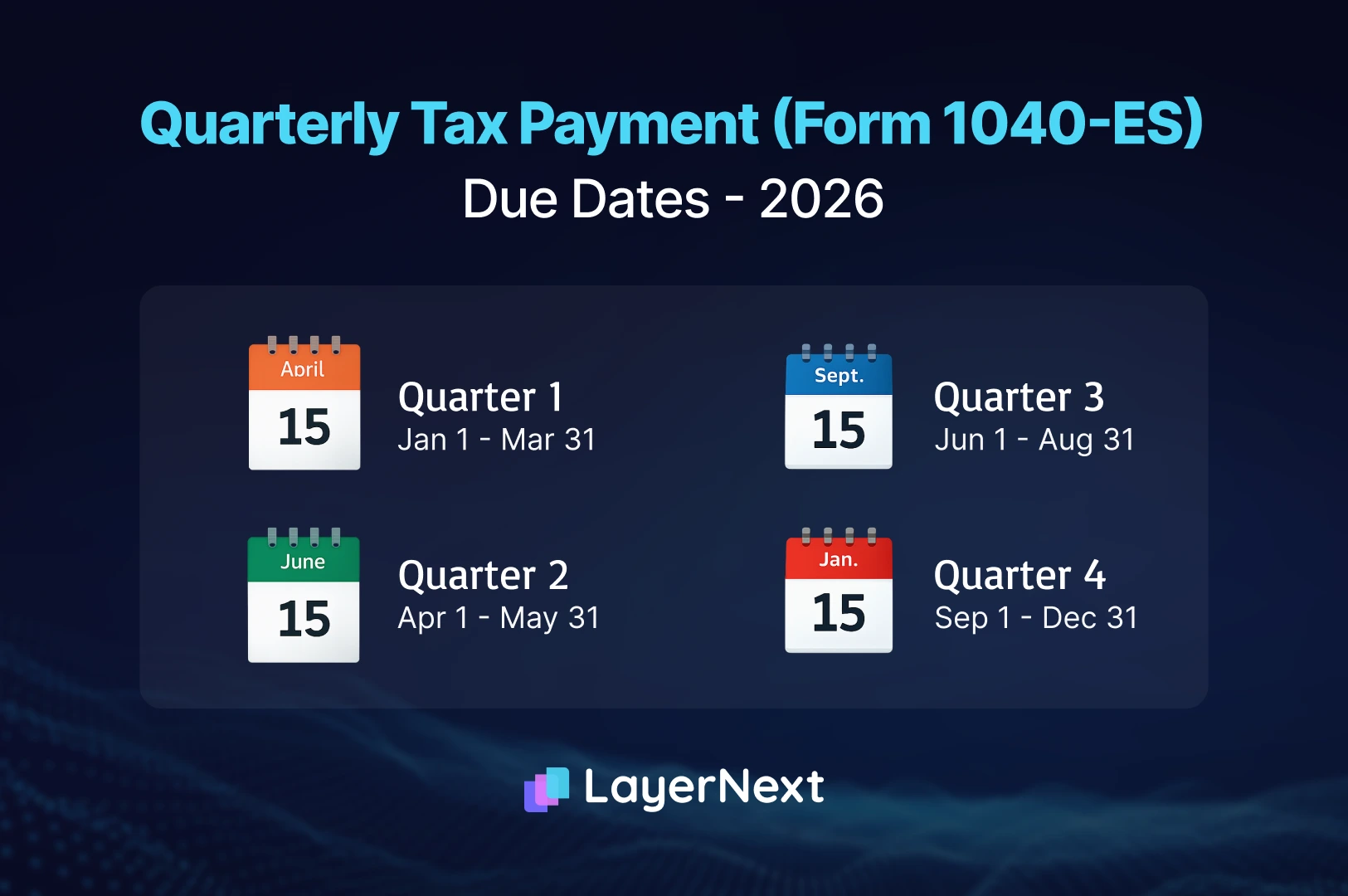

Quarterly Estimated Tax Payment Deadlines for 2026

Quarterly payment deadlines are fixed, and missing them can lead to penalties. Here are the 2026 deadlines:

*June 15, 2026 falls on a Monday; deadline remains June 16, 2026.

Important: If a due date falls on a weekend or federal holiday, the deadline moves to the next business day.

These deadlines apply to federal estimated taxes; state deadlines may differ.

IRS deadline reference: https://www.irs.gov/businesses/small-businesses-self-employed/estimated-taxes

Adjusting Estimated Taxes During the Year

Estimated tax payments are not set in stone. You can and should recalculate them if your financial situation changes.

Common reasons to adjust payments include:

- A significant increase or decrease in income

- Landing a new contract or losing a major client

- Major changes in deductible expenses

- Moving from a loss to a profit (or vice versa)

- Unexpected medical expenses or large purchases

Revisiting estimates quarterly helps prevent underpayment and large year-end balances.

What If Your Income Is Irregular or Seasonal?

If your income is uneven or seasonal (common for consultants, retailers, or service providers), dividing estimated tax evenly across four quarters may not reflect reality.

The IRS allows the annualized income method, which bases payments on income earned during each specific period rather than a flat estimate. This can be useful for businesses with fluctuating revenue.

Annualized income method overview: https://www.fidelity.com/learning-center/smart-money/estimated-tax-payments

How to Pay Quarterly Estimated Taxes

You can submit payments in several ways. Electronic payments are generally faster, more secure, and easier to track.

Online Payment Options (Recommended)

- IRS Direct Pay (free bank transfer)

- EFTPS (Electronic Federal Tax Payment System)

- IRS2Go mobile app

- Debit or credit card (convenience fees apply, typically 1.87-1.99%)

IRS payment options: https://www.irs.gov/payments

Paying by Mail

You can mail a check with the appropriate payment voucher from Form 1040-ES. Allow extra time for processing, and send via certified mail for proof of payment.

What Happens If You Miss a Quarterly Tax Payment?

If you miss a payment or underpay:

- The IRS may assess penalties and interest

- Interest compounds daily on unpaid amounts

- Penalties are calculated based on how much you underpaid and for how long

Current IRS underpayment penalty rate: Generally tied to the federal short-term rate plus 3%

If you discover a missed payment, paying as soon as possible and adjusting future estimates can help limit additional charges.

What happens when a payment is missed: https://www.bpm.com/insights/what-happens-if-you-miss-quarterly-estimated-tax-payment/

Using Last Year's Tax Return as a Starting Point

If estimating current-year income feels difficult, last year's tax return can serve as a practical baseline.

Using prior-year tax figures can:

- Reduce the risk of underpayment

- Simplify planning

- Work well alongside safe harbor rules

Simply take your total tax from line 24 of your 2025 Form 1040, divide by 4, and pay that amount quarterly. This approach qualifies for safe harbor protection.

IRS guidance on using prior-year taxes: https://www.irs.gov/businesses/small-businesses-self-employed/estimated-taxes

Real-World Calculation Example

Let's walk through a practical example:

Sarah's Situation:

- Freelance graphic designer

- Expected 2026 income: $80,000

- Business expenses: $15,000

- Net business income: $65,000

Step-by-Step Calculation:

- Net self-employment income: $65,000

- Self-employment tax: $65,000 × 92.35% = $60,028 (taxable for SE tax)

- SE tax = $60,028 × 15.3% = $9,184

- Deduction for half of SE tax: $9,184 ÷ 2 = $4,592

- Adjusted gross income: $65,000 - $4,592 = $60,408

- Standard deduction (2026): $14,600

- Taxable income: $60,408 - $14,600 = $45,808

- Federal income tax (2026 rates): ~$5,290

- Total tax liability: $5,290 + $9,184 = $14,474

- Quarterly payment: $14,474 ÷ 4 = $3,619 per quarter

Common Mistakes Entrepreneurs Make with Quarterly Taxes

1. Forgetting About Self-Employment Tax

Many first-time entrepreneurs only calculate income tax and forget the 15.3% self-employment tax. This can result in significantly underpaying.

2. Not Adjusting After a Big Income Change

Landing a major contract mid-year? Your original estimate is now outdated. Recalculate and increase remaining payments.

3. Missing the June Deadline

The second quarter deadline (June 15/16) catches many people off guard because it only covers two months of income, not three.

4. Paying Late But Not Immediately

If you miss April 15, don't wait until June 15. Pay as soon as possible to minimize penalties.

5. Not Keeping Records

Always keep confirmation numbers, receipts, and payment records. Electronic payments automatically create a paper trail.

State Estimated Tax Requirements

Most states with income tax also require quarterly estimated payments. State deadlines typically mirror federal deadlines, but not always.

States with different requirements:

- Delaware: Different due dates

- Louisiana: Different due dates

- Iowa: Different due dates

Check your state's department of revenue website for specific requirements.

Practical Tips for Managing Quarterly Taxes

- Set up a separate tax savings account: Automatically transfer 25-30% of each payment you receive into a dedicated account

- Review estimates quarterly: Don't just set and forget reassess every three months

- Use accounting software: Tools like QuickBooks, FreshBooks, or Xero can track income and expenses in real-time

- Set calendar reminders: Add due dates to your calendar with a one-week advance warning

- Work with a tax professional: A CPA or EA can help optimize deductions and ensure accuracy

- Keep financial records current: Don't wait until the end of the quarter to update your books

- Consider safe harbor: When in doubt, use the prior-year safe harbor method to avoid penalties

How Modern Financial Tools Simplify Quarterly Tax Planning

Quarterly estimated taxes rely on one thing above all else: accurate, up-to-date financial data.

Modern AI-powered accounting platforms act as virtual CFOs by keeping your books clean, current, and tax-ready throughout the year. Automated transaction categorization, reconciliation, and real-time financial insights help you clearly understand income, expenses, and cash flow as they happen.

That clarity makes quarterly tax planning far more manageable. Instead of estimating based on outdated numbers or rough guesses, you're working from real data every time a payment is due.

Key features that help with quarterly taxes:

- Real-time profit and loss tracking: Know exactly how much you've earned

- Automated expense categorization: Ensure you're capturing all deductions

- Cash flow forecasting: Plan for upcoming tax payments without surprising yourself

- Integration with tax software: Export data directly to TurboTax, TaxAct, or your CPA

With the right tools, quarterly estimated taxes become a planning exercise not a last-minute scramble.

Final Thoughts

Quarterly estimated taxes don't have to be overwhelming, but they do require consistency and awareness. Once you understand who needs to pay, how estimates are calculated, and when payments are due, the process becomes far more manageable.

The biggest mistakes usually come from outdated numbers, missed deadlines, or not adjusting estimates as income changes. Staying proactive—reviewing your finances regularly and recalculating when needed—can help you avoid penalties and year-end surprises.

With the right systems in place and a clear understanding of Form 1040-ES, quarterly tax payments become part of your routine rather than a source of stress. A little preparation each quarter goes a long way toward keeping your business compliant, cash-flow stable, and focused on growth instead of tax headaches.

Remember: The IRS prefers you to overpay slightly throughout the year rather than underpay. You'll get any overpayment back as a refund, but underpayment comes with penalties and interest.

Start with conservative estimates, track your actual income quarterly, adjust as needed, and you'll master the quarterly tax process in no time.

Additional Resources:

- IRS Form 1040-ES: https://www.irs.gov/forms-pubs/about-form-1040-es

- IRS Payment Portal: https://www.irs.gov/payments

- Self-Employment Tax Center: https://www.irs.gov/businesses/small-businesses-self-employed/self-employed-individuals-tax-center

- Estimated Tax Guide: https://www.irs.gov/businesses/small-businesses-self-employed/estimated-taxes

Disclaimer: This article is for educational purposes only and does not constitute tax, legal, or financial advice. Tax laws are complex and subject to change. Please consult with a qualified tax professional or financial advisor to discuss your specific situation and ensure compliance with current regulations.