Summary

Paying yourself as an S Corporation owner requires a balance between compliance and tax efficiency. The IRS mandates that active owners take a reasonable salary before distributions. Getting this right helps you reduce tax liability while avoiding penalties.

Key Takeaways:

- You must pay yourself a reasonable salary if you actively work in your S Corp

- Salary is subject to payroll taxes, but distributions are not

- Skipping salary is a major IRS audit trigger

- Proper payroll setup and documentation are essential

- A balanced salary and distribution strategy can reduce overall tax burden

If you run a business as an S corporation, the way you pay yourself is not optional. It is a legal obligation governed by IRS rules and decades of Tax Court precedent. Many business owner select S corp status specifically to reduce self-employment taxes, but that strategy is only legal when paired with a legitimate salary. Understanding exactly what the IRS demands, and how to satisfy it, can mean the difference between a clean tax return and a costly audit.

The Core Rule: Reasonable Compensation Is Mandatory

An S corporation is a pass-through entity, meaning its profits flow to shareholders and are reported on their individual tax returns. Unlike a sole proprietor, an S corp owner-employee does not owe self-employment tax on all business profits, only on wages. This creates an obvious temptation: take a zero salary and pocket everything as distributions, which avoid payroll taxes entirely.

The IRS is fully aware of this strategy and expressly forbids it. Under IRC Section 3121 and related caselaw, any shareholder who performs services for an S corporation must be treated as an employee and paid a salary that reflects the fair market value of those services. This is called "reasonable compensation."

IRS Enforcement Note

The IRS has prevailed repeatedly in Tax Court against S corp owners who paid themselves little or no salary. In Watson v. Commissioner (2012), the Eighth Circuit Court of Appeals upheld the IRS's recharacterization of distributions as wages, resulting in significant back payroll taxes, interest, and penalties. The court found that a $24,000 salary on $200,000+ in profit was unreasonably low.

Who Is Required to Take a Salary?

Not every S corp owner triggers the salary requirement. The rule applies specifically to shareholder-employees, meaning owners who actively work in the business.

If your business has multiple shareholders and some are purely passive investors who never perform services, those individuals do not need a salary. But any shareholder who manages operations, performs client work, or materially participates in running the business is subject to the reasonable compensation requirement.

What Is Reasonable Compensation?

Reasonable compensation is not defined by a single fixed number. It is a facts-and-circumstances standard that asks: what would you have to pay a third-party employee to perform the same services? The IRS uses several factors drawn from court decisions to evaluate this, including:

- Training, experience, and duties of the shareholder-employee

- Time and effort devoted to the business

- What comparable businesses pay for similar roles in the same market

- Gross revenues and net profits of the corporation

- Whether compensation is consistent year over year

- What the S corp paid non-shareholder employees in similar roles

- Economic conditions in the industry and region

Practical Benchmark

Many tax professionals reference a 60/40 approach as a starting point: roughly 60% of net profit paid as salary and 40% as distributions. This is not an IRS-approved formula, and the actual split should reflect the market rate for your specific role. The best evidence is documented salary benchmarking from credible sources such as the Bureau of Labor Statistics or industry compensation surveys.

How Salary and Distributions Work Together

Once you understand the requirement, the compensation structure for an S corp owner-employee works as follows:

Salary (W-2 wages): You pay yourself a reasonable salary. The S corp withholds and remits payroll taxes (FICA: 7.65% employee share, 7.65% employer share, for a combined 15.3% up to the Social Security wage base). The salary is a deductible business expense for the S corp.

Distributions: After paying a reasonable salary, remaining profits can be distributed to shareholders on a pro-rata basis according to ownership percentage. Distributions are not subject to FICA payroll taxes. They are passed through to shareholders as ordinary income on Schedule K-1 (Form 1120-S) and reported on the individual return.

The tax savings of an S corp come from this distribution tier. Those savings are only available after a legitimate salary has been paid. Taking all profits as distributions with no salary is not a tax strategy; it is a violation of IRS rules.

A Concrete Example

Suppose your S corp earns $180,000 in net profit and you are the sole owner-employee. A reasonable salary for your role might be $90,000. Here is how different approaches compare:

The third scenario is the target: a defensible reasonable salary that leaves room for tax-advantaged distributions.

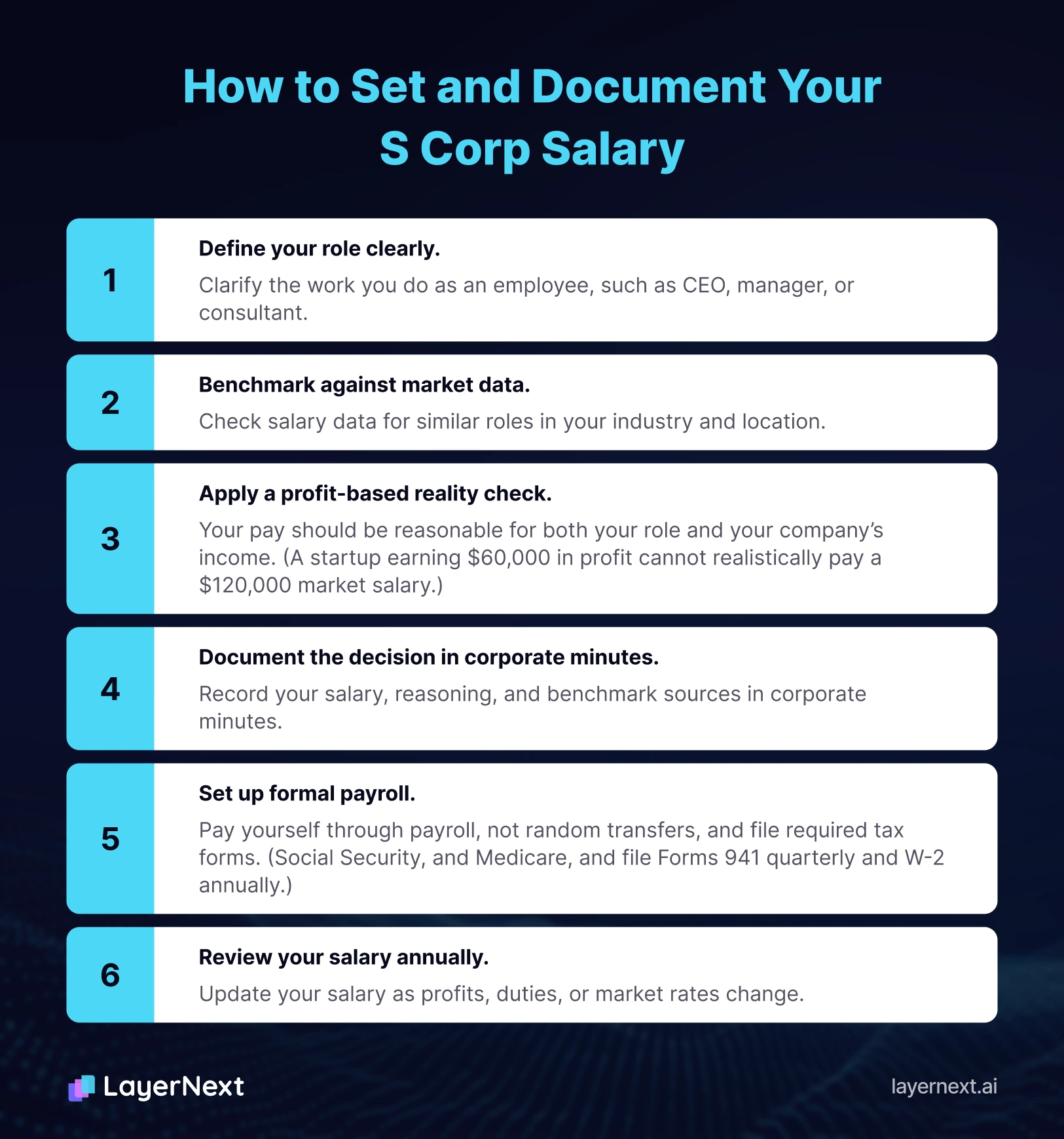

How to Set and Document Your S Corp Salary

Setting a compliant salary is both a financial exercise and a documentation exercise. The IRS will not simply take your word for it. You need evidence that your salary reflects market rates.

- Define your role clearly.

Write a job description for the work you perform in the business, not as an investor or owner, but as an employee (for example: CEO, operations manager, lead engineer, or licensed professional). - Benchmark against market data.

Use sources such as the Bureau of Labor Statistics Occupational Employment and Wage Statistics, Salary.com, or industry-specific compensation surveys to find median compensation for your role in your geography. - Apply a profit-based reality check.

Courts consider the company's ability to pay. A startup earning $60,000 in profit cannot realistically pay a $120,000 market salary; the salary must be both reasonable and sustainable. - Document the decision in corporate minutes.

Your board resolution (even as a sole owner) should formally establish the salary, the rationale, and the benchmarks used to support that figure. - Set up formal payroll.

Reasonable compensation must flow through a proper payroll system, not informal transfers. You must withhold federal and state income taxes, Social Security, and Medicare, and file Forms 941 quarterly and W-2 annually. - Review your salary annually.

As your business grows, your salary should be revisited. A salary that was reasonable three years ago may invite scrutiny if profits have grown substantially and compensation has not changed.

What Happens If You Do Not Pay Yourself a Salary?

The IRS has broad authority to reclassify distributions as wages when it determines a shareholder-employee failed to receive reasonable compensation. When this happens:

- Back payroll taxes are assessed, covering both the employee and employer portions of FICA (up to 15.3%).

- Failure-to-deposit penalties apply, ranging up to 15% of the unpaid payroll taxes.

- Interest accrues from the original due date of the payroll tax deposits.

- Accuracy-related penalties of 20% may be added if the underpayment is deemed substantial.

- State payroll tax liabilities may also be triggered, depending on your state.

Red Flags That Invite IRS Scrutiny

The IRS looks for patterns such as: the only shareholder takes no salary; distributions are disproportionately large relative to the salary; the salary drops sharply as profits rise; or the salary is set at a suspiciously round number with no market justification.

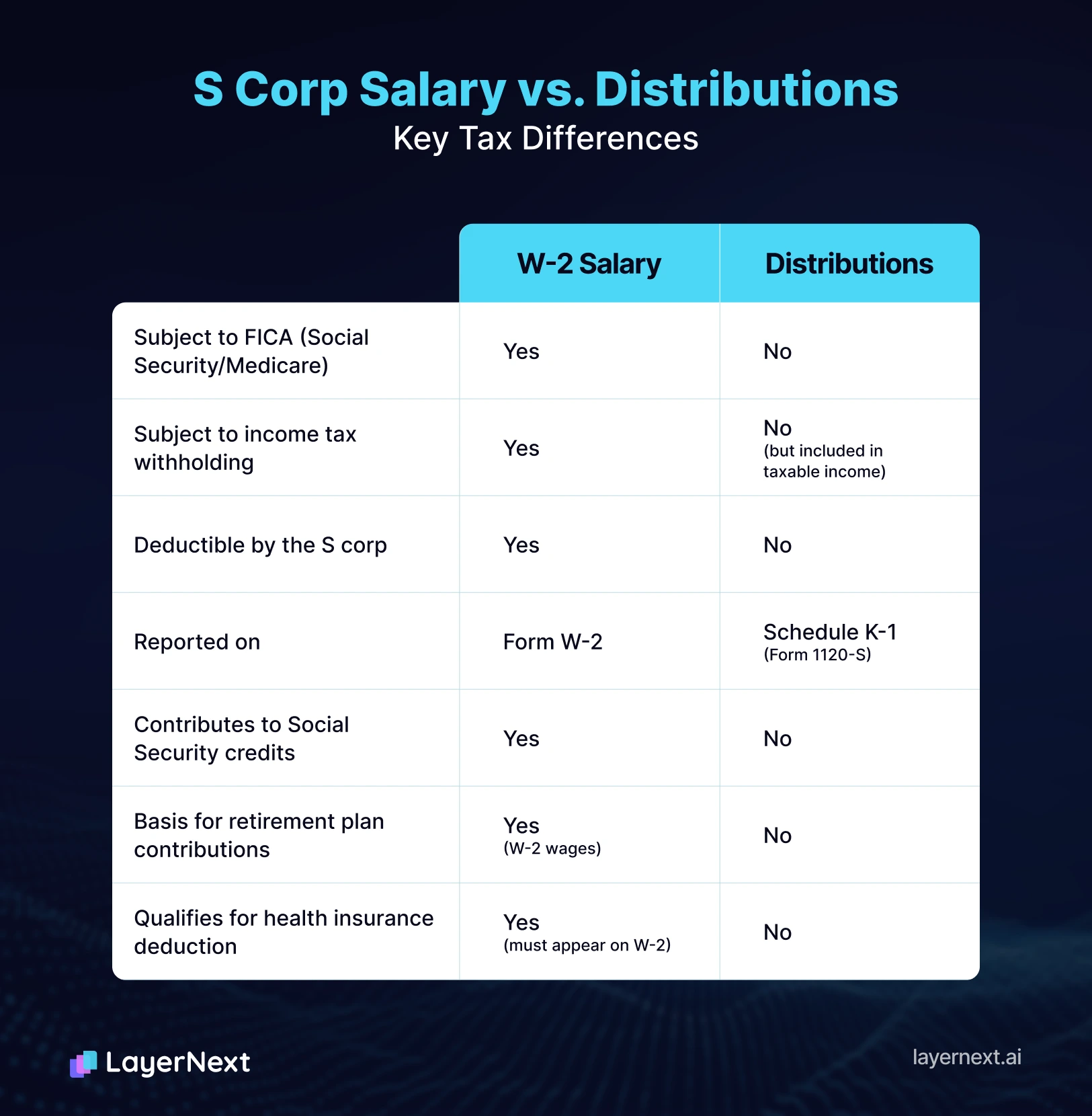

S Corp Salary vs. Distributions: Key Tax Differences

This comparison highlights an often-missed point: your salary is not just a tax obligation. It is the foundation for other benefits. Solo 401(k) contributions, self-employed health insurance deductions, and SEP-IRA contributions are all tied to your W-2 compensation. Setting your salary too low does not just invite IRS scrutiny; it also limits your retirement and benefits planning.

Special Situations

Single-Owner S Corps

A single-shareholder S corp must still pay a reasonable salary. The IRS does not grant an exemption because you are the sole owner. In fact, single-owner S corps can receive heightened scrutiny precisely because there is no arm's-length relationship to set compensation at market rates.

Part-Time or Startup-Phase Businesses

If your S corp is in early stages and genuinely not generating enough profit to support a salary, the IRS acknowledges this practical constraint. An S corp paying no salary during a loss year is far less problematic than a profitable business deliberately avoiding payroll. Once the business is profitable and you are actively working in it, the reasonable compensation obligation applies regardless of how long the business has been operating.

Owner-Employee Health Insurance

Health insurance premiums paid by the S corp for a more-than-2% shareholder-employee must be included in Box 1 of the W-2 as wages, then deducted on the shareholder's individual return via Form 1040, Schedule 1. This is a common reporting error. The premiums do not bypass W-2 reporting. Per IRS Notice 2008-1, this treatment is required for the shareholder to claim the self-employed health insurance deduction.

Stop Managing Bookkeeping Manually

LayerNext automates everything your bookkeeper used to do, so you can focus on running your S corp.

Getting your S corp salary right is only half the equation. The other half is keeping your books clean, your payroll reconciled, and your financials tax-ready year-round. That is exactly what LayerNext is built to do.

LayerNext is an AI CFO platform built for small business owners. It connects directly to QuickBooks, automatically categorizes every transaction, reconciles your bank feeds in real time, and delivers CFO-level insights including cash flow, burn rate, and runway, without requiring you to touch a spreadsheet or chase down receipts.

What LayerNext Does for S Corp Owners

- Autonomous bookkeeping

Every expense, invoice, and receipt is automatically captured and categorized. No manual entry, no month-end chaos. - Real-time bank reconciliation

Connect your bank feeds or upload statements. LayerNext matches and reconciles every transaction automatically, the same way a skilled accountant would. - CFO-level financial insights

Instant visibility into cash flow, burn rate, and runway. Smart tax-saving tips surfaced automatically so you are never making financial decisions in the dark. - Always-closed books

Your books are up to date at all times, not just at year-end. When your accountant or the IRS asks for records, they are already ready.