Overview | Financial Insights Guide

LayerNext can generate financial insights directly from your financial data connected such as QuickBooks and help you make informed business decisions. It goes beyond simple answers by analyzing trends, comparing periods, and identifying the key drivers behind changes in your numbers. The guidelines below show how to structure prompts so LayerNext can deliver accurate, evidence-based insights and actionable next steps.

The guidelines below show how to structure prompts so LayerNext can deliver accurate, evidence-based insights and actionable next steps.

1. Start with the decision you’re trying to make

Instead of “Why is revenue down?”, tell the AI what you want to decide and what “good” looks like.

Better

2. Add a timeframe and a comparison baseline

Insights get much stronger when the AI knows when and compared to what. Include:

- Period (e.g., “Dec 2025”)

- Baseline (e.g., “vs Nov 2025” or “vs Dec 2024”)

- Granularity (weekly/monthly)

Better

3. Tell it how to break the problem down (dimensions + metrics)

Give the “cuts” you care about, and which metrics matter.

Common dimensions:

- Product/service, customer, channel, region, invoice vs cash, new vs existing customers, one-time vs recurring, classes/locations/projects (if used)

Common metrics:

- Revenue, volume (# invoices), average invoice value, discount rate, churn/retention, AR aging, gross margin

Better

4) Provide business context and constraints (so it reasons like your finance partner)

LLMs do better when they know what changed operationally.

Examples of context to include:

- Price changes, promos, lost customer, seasonality, capacity constraints, delayed projects, staffing changes, inventory/parts issues, policy changes, product launch, billing changes

- Constraints: “don’t recommend hiring,” “we can’t change price this quarter,” etc.

Better

5) Ask for an evidence-based output (ranked drivers + checks + actions)

Tell the AI to show its work using QuickBooks-backed evidence and to sanity-check conclusions.

Ask for:

- Top drivers ranked by $ impact

- Supporting tables (top movers)

- Data quality checks (coding changes, duplicates, misclassified income, timing issues)

- Clear actions and what to monitor next

Better

These are some sample insights that can be generated from QuickBooks Data.

Example Question 1

Answer

Overall Cashflow Trend

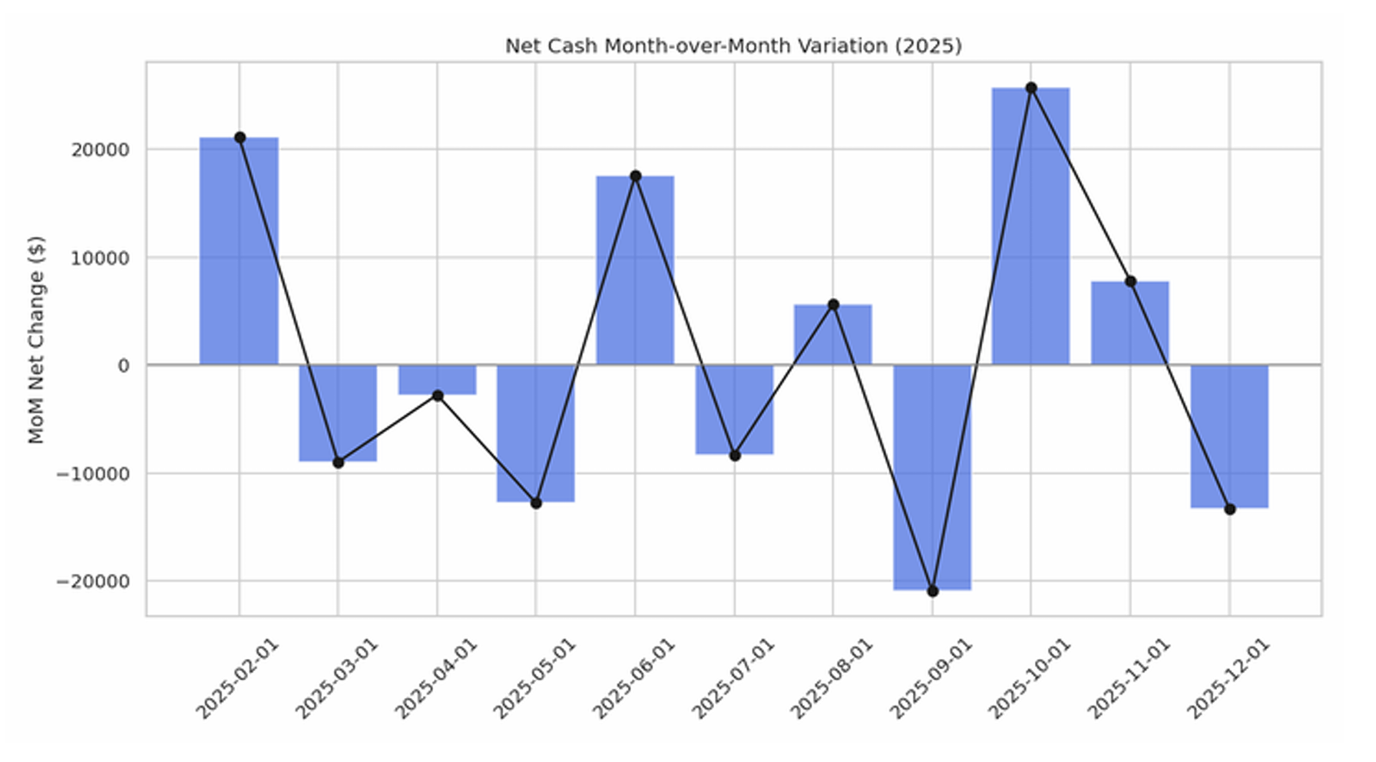

The business experienced wide swings in net cash during 2025:

- Largest net outflow in September (-$24.5 k) driven by a spike in cash-out.

- Strongest net inflow in February (+$6.2 k) as cash-out was unusually low.

- Month-over-month variability reached ±$21 k, revealing inconsistent liquidity needs. Major expense categories contributing to cash-out

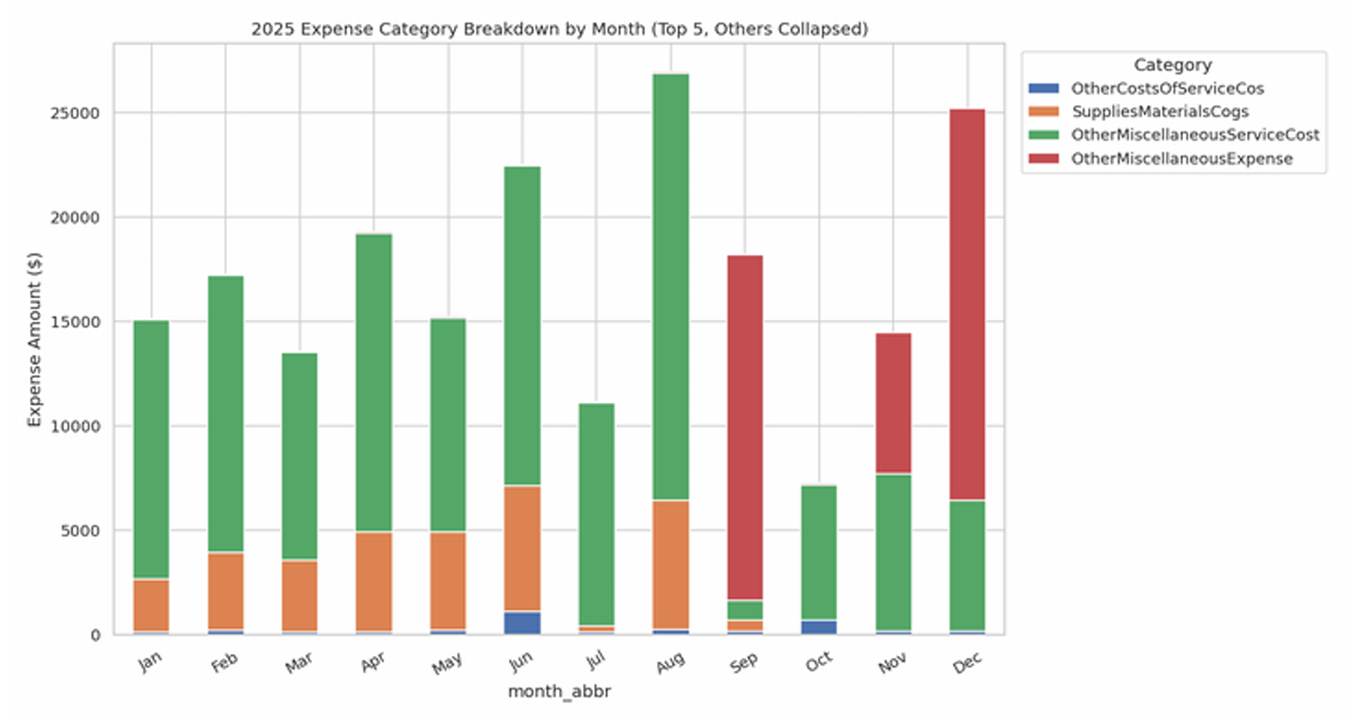

Major expense categories contributing to cash-out

Key findings:

- Other Miscellaneous Service Cost was the dominant cash-out driver (≈ $128 k), peaking in Jan, Jun and Aug.

- Other Miscellaneous Expense contributed $42 k, with heavy outflows in Sep and Dec.

- Supplies / Materials COGS ($32 k) spiked mid-year (May–Aug) aligning with production needs.

- Remaining costs (e.g., Other Costs of Service) were comparatively minor (< $4 k annually). Drivers of monthly cash-flow variations

Drivers of monthly cash-flow variations

- February improvement (+$21 k MoM) – cash-out dropped to $12.8 k while inflows stayed steady; no major category surge.

- March–May decline (-$21 k cumulative) – rising Supplies/Materials and service costs pushed cash-out to double inflow.

- June rebound (+$17 k) – cash-out normalised while inflow climbed, easing liquidity.

- September trough (-$21 k MoM) – one-off Miscellaneous Expense payment ($16.5 k) plus elevated service costs drove record outflow.

- October recovery (+$25 k) – outflow fell sharply, restoring positive net cash despite moderate inflows.

Summary

2025 cash-flow was highly volatile. Miscellaneous service costs dominated spending, accounting for ~60 % of annual cash-out. Monitoring these discretionary costs and smoothing payment timing could stabilise liquidity. September’s outsized outflow warrants review to confirm it was a planned one-off expense.

Followup Question

Answer

September 2025 Cash-Out Deep-Dive

1.Biggest individual cash-out transactions

- Two purchase payments on 21-Sep ($17.2 k) and 22-Sep ($14.6 k) together drove 69 % of the month’s spending.

- Two credit-card payments (21-Sep & 15-Sep) added another $12.7 k.

- All transactions posted to the Chase Checking account; remaining outflows were immaterial.

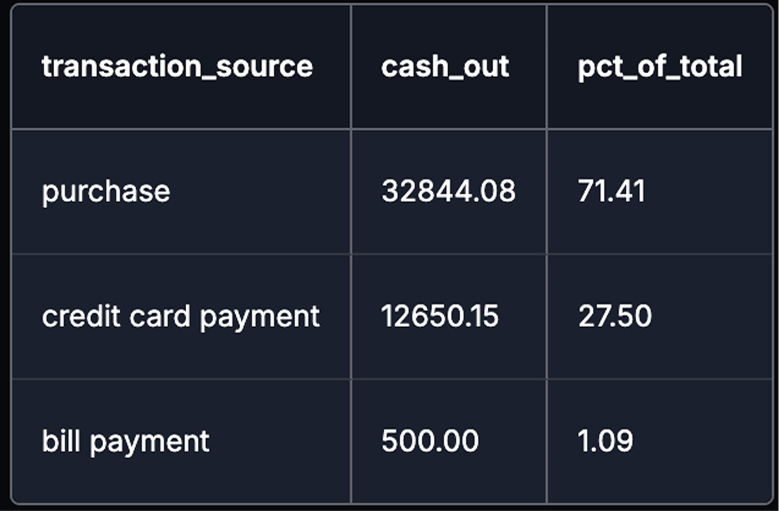

2.Cash-out by transaction source

- Purchases – $32.8 k (71.4 %)

- Credit-card payments – $12.7 k (27.5 %)

- Bill payment – $0.5 k (1.1 %)

3. Reason for the September spike The unusually high September cash-out (-$24.5 k net) is almost entirely due to two large purchase disbursements plus a lump-sum credit-card payoff. No unusual bill-payment or transfer activity was detected. Controlling large purchase approvals and smoothing credit-card payments could prevent similar spikes.

Example Question 2

Answer

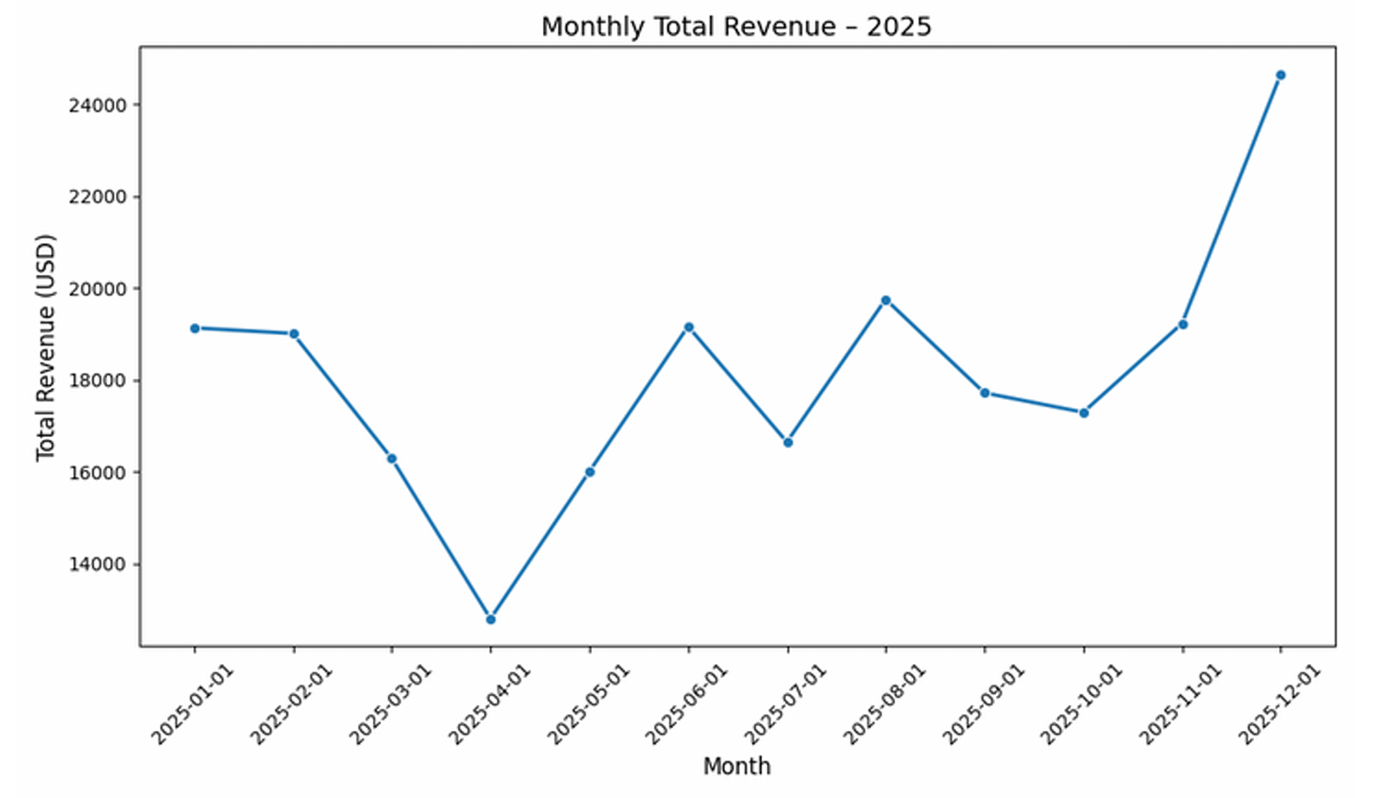

Overall Monthly Revenue Trend

The line chart shows total revenue by month. After a low point in April, revenue rebounded steadily and reached its peak in December.

Revenue by Class

A stacked-bar view highlights how each revenue class contributed throughout the year.

Key insights:

- Petkinns/SOYSAND (Shopify) dominated 2025, accounting for 84.7 % of annual revenue.

- Kidloot (FBA) represented 14.2 %, providing a stable secondary stream.

- Kinn Furniture (TBD) contributed just over 1 %.

- Seasonal surges are evident in November–December, driven mainly by the Shopify class.

Followup Question

Answer

1. Month-over-Month Growth Pattern

The chart below tracks the percentage change in revenue from one month to the next.

Highlights

- Sharp declines in March (-14 %) and April (-21 %) set a low baseline.

- Recovery begins in May and June, then dips again in July and September.

- The decisive jump comes in December (+28 %), the highest single-month lift of the year.

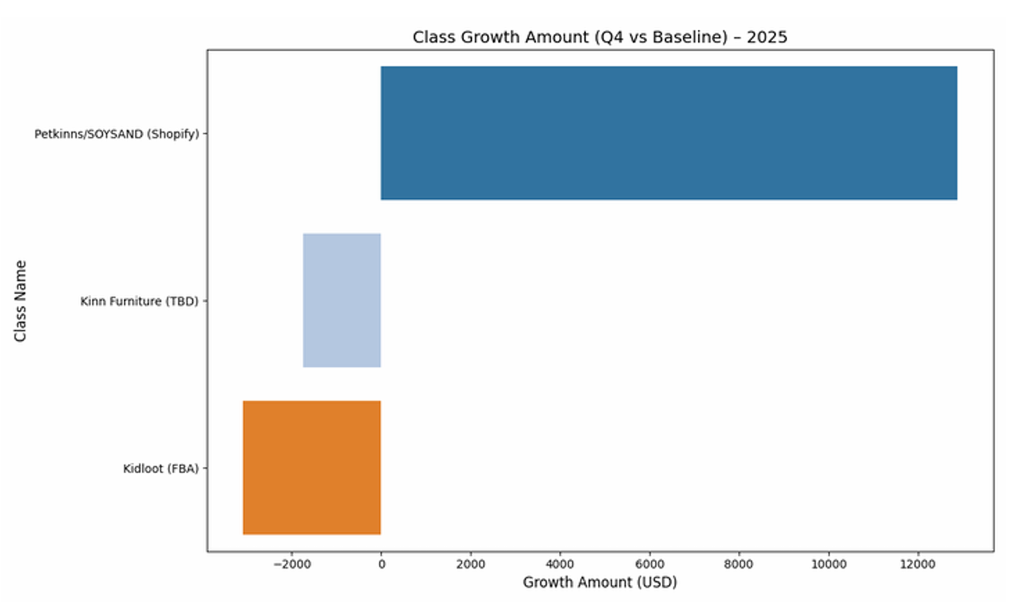

2. Which Revenue Sources Fueled Q4 Growth?

To isolate year-end drivers we compared Q4 totals (Oct–Dec) with the average monthly revenue from January–September for each class.

Key findings

- Petkinns/SOYSAND (Shopify) generated an additional $12.9 k over its Jan–Sep baseline, accounting for >100 % of net growth. All other classes contracted in Q4.

- Kidloot (FBA) slipped by $3.1 k versus baseline, diluting overall gains.

- Kinn Furniture showed negligible sales earlier and dropped to zero in Q4.

3. Interpreting the Surge

- Shopify promotions & seasonal demand – The Shopify class (Petkinns/SOYSAND) likely ran holiday campaigns or benefited from Q4 e-commerce seasonality. Its sales rose ~39 % above baseline each month in Q4.

- Channel concentration – Because Shopify now represents ~85 % of annual revenue, any promotion there disproportionately lifts totals.

- Limited contribution from other classes – FBA and Furniture lines did not participate in the Q4 uplift; in fact they contracted, implying inventory issues or strategic deprioritisation.

4. Recommendations

- Double-down on proven Q4 Shopify tactics—evaluate which campaigns/products delivered the lift.

- Mitigate concentration risk by revitalising Kidloot (FBA) or diversifying new channels.

- Plan inventory and marketing for October launches to capture momentum earlier, smoothing the steep December spike.